Macroeconomics of twin-targeting in Turkey: analytics of a financial computable general equilibrium model

Tam metin

Şekil

Benzer Belgeler

bezekler stilistik yöntemlerle inccknerek s~n~fiand~nlmglard~r, sonras~nda Le~. olmak üzere 3 farkl~~ evrenin varl~~~~ ortaya konulmu~tur. yy.'a wanan süreçtek~~ Geç Antik

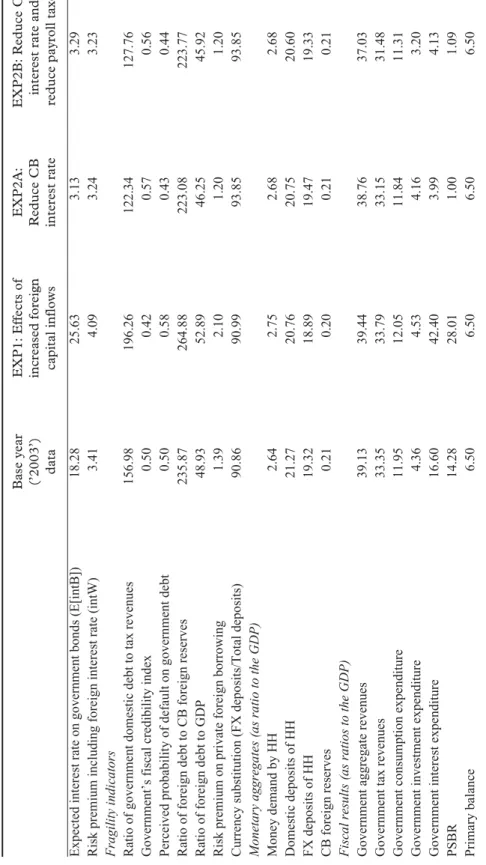

In the opposite, with the increase in the military expenditures, the shifting budget from government saving to defense spending result in deterioration of the

Changes in the amino acid sequence in the variable region of the heavy and light chain of the Ig molecule. Determines

Mahmut Cûda'nın 1980 de İzmir Resim ve Heykel Müzesi’ndeki sergisini görünce o resim gerçek bir ipucu oldu.I. Ama araç olarak seçtiği nesneleri büyük bir ustalık,

Marmara kıyalarında ve bu masmavi gökler ve bol güneşli günler le bazan aylı ve to zan keljkeşanlı ge celer Silimi olan Tahkiyem izde

Bu dönüşler jimnastik mi ki, banda alıyorlar, onları Allah döndürüyor» diyen Mevlevi tekke lerinin arda kalanlan, bir yandan evlerde yer yer coşkulu

Aşağıdaki sayıların kendinden önceki ve sonraki 100’ün katı olan sayıları yazın ve hangisi- ne daha yakın ise o sayıyı işaretleyin.. a)

Y etiştirdiği sayısız öğrenci - le r arasında bugün Ankara Devlet Balesinin ünlü isim - le ri olan Tenasüp Onat, Gü zide N oyan, Hüsnü Sunal, Su - na Bayer