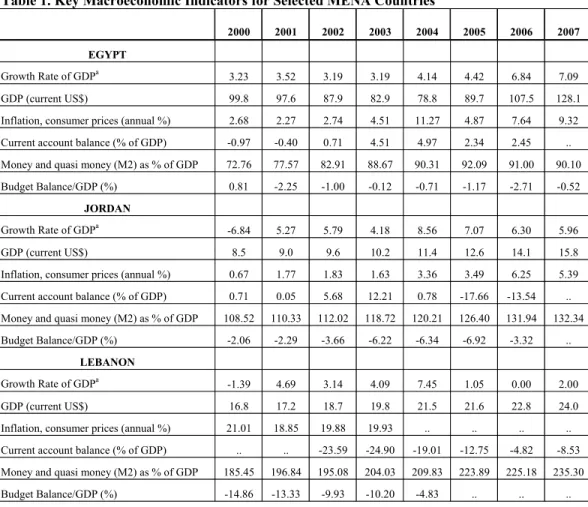

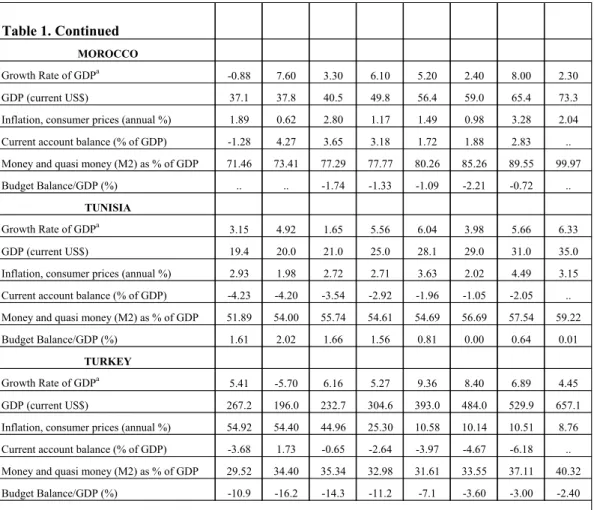

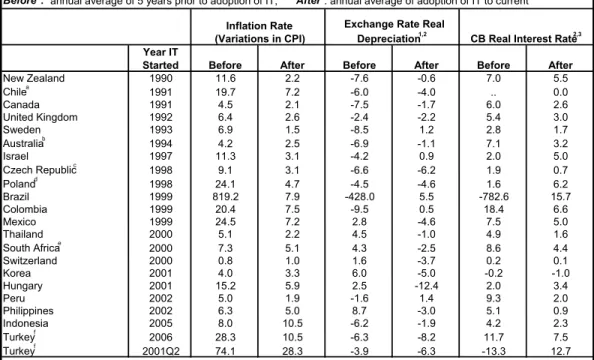

Prospects for inflation targeting in the MENA region: feasibility, desirability and alternatives

Tam metin

Şekil

Benzer Belgeler

The Oberlin-Wellington rescue case grew out of a rescue party’s release of a fugitive slave in 1858 in Oberlin, Ohio; the slave had been in the custody of a federal officer at

In Section 3, we project out the flow variables in the hub location formulation and characterize the extreme rays of the projection cone for a single

The status of Syrian Kurds, the political future of Bashar al Assad, the presence of Turkish forces in Northern Syria, divergent positions over Idlib and Russia’s ties with Iran

Dünyadaki dağılışı: Avrupa’nın sıcak kesimleri, Filistin, Güney Almanya, Orta Fransa’ ya kadar olan kesim, Kafkasya, Kuzey Sibirya, Sovyet Uzak Doğu, Türkiye, Ukrayna,

We have discussed some characteristics of computer aided education, the user interface, tools of the user interface, notification based systems, and object

Many tools are used in the construction of expert systems. Those tools range from general purpose languciges such as LISP to highly specialized expert system

In this paper, we show that CMUT performance under continuous wave drive signal can be maximized by considering the radiation impedance of the transducer and operating transducer

Pictorial Oculomotor Binocular Motional Occlusion Accommodation Binocular disparity Motion parallax Cast shadow Convergence Motion perspective Linear perspective Kinetic depth