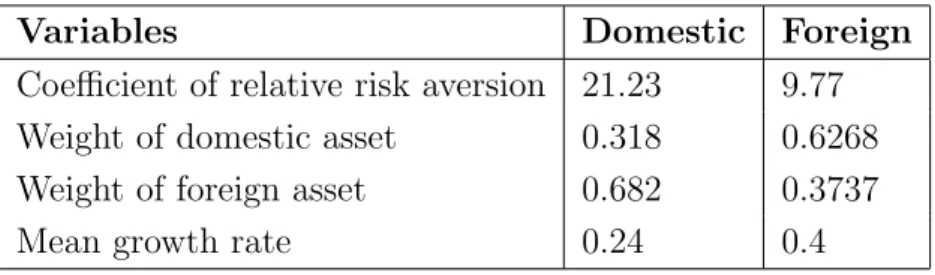

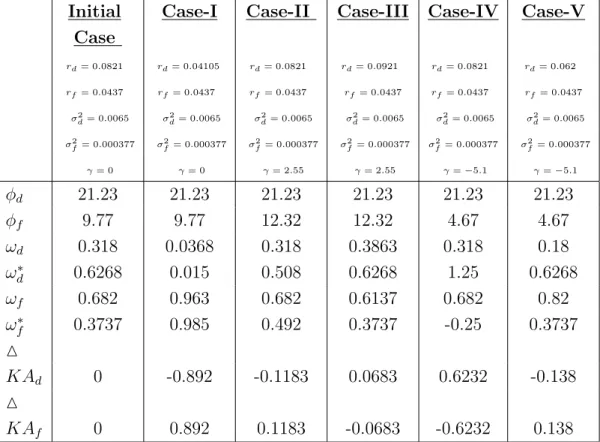

Role of risk aversion in countries' portfolio choices

Tam metin

Şekil

Benzer Belgeler

As a result of long studies dealing with gases, a number of laws have been developed to explain their behavior.. Unaware of these laws or the equations

I Solve for the unknown rate, and substitute the given information into the

«Life the hound» (from «The Hound» by Robert Francis) Life – literal term, hound – figurative term.. • In the second form, the literal term is named and the figurative term

According to the Republican Medical Informational Centre (1) in the Kyrgyz Republic in 2007 the cardiovascular diseases take the first place in structure of the general death

The aim of this study is to examine the relationship between average annual crude oil price (nominal value in USD), gross domestic product (2010 prices and $) and export (2010

According to Léon-Ledesma and Thirlwall (2002), the endogeneity of the natural growth rate means that full employment ceiling is not constant; it can increase und er

Oktay Akbaş (Doç. Dr., Kırıkkale Üniversitesi) Nurullah Altaş (Prof. Dr., Atatürk Üniversitesi) Mustafa Arslan (Prof. Dr., İnönü Üniversitesi) Ednan Aslan (Prof. Dr.,

Ce lâl Esat Arseven gibi yalnız dilci değil aynı zamanda üze rinde uğraştığı mefhumların spesiyalisti olan ve üstelik iyi yazıcı olarak, bu