Foreign direct investment in Turkey: regional determinants

Tam metin

Şekil

Benzer Belgeler

Trabzon Numune Hastanesi’nin 20 yataklı Çocuk Servisi’ne grip, is hal, bronşit ve sarılıktan 33 çocuk yatınldı. Bir yatağa iki çocuk ya tırmak

O anlayış, o konuşuş, o çalışış, o tavır, o eda -ki şarkın Türkiyesiydi, tevekkül gibi görünen isyandı, mah viyet gibi görünen gururdu, sükûnet

Birinci şa hıs, nasıl üçüncü şahsa sığınmış, giz lenmişse, Behçet Necatigil kendi ö- züyle, kişiliğiyle bir takım maddelere gizlenmiştir.. Daha

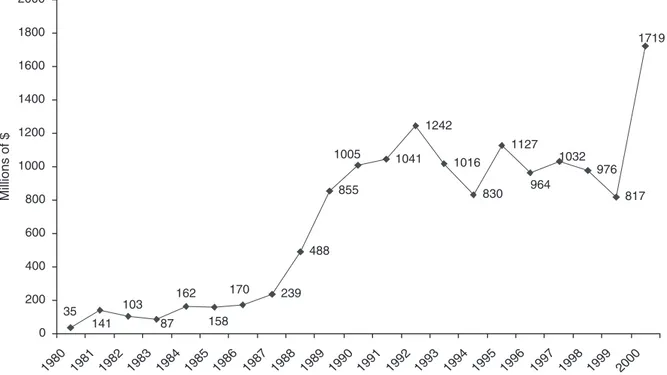

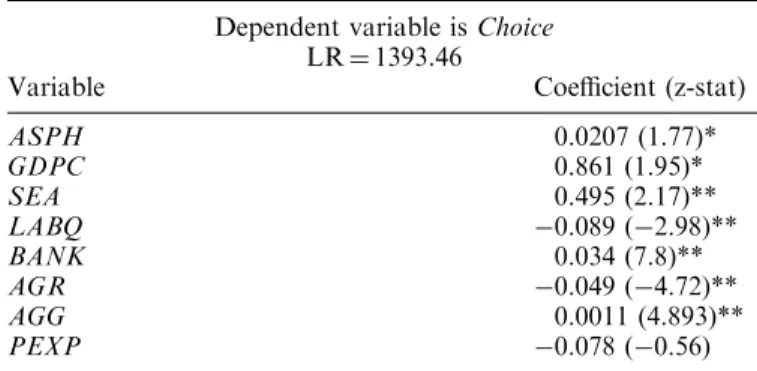

In his research, Bosut (1999) describes Turkey as a large and growing domestic market for the foreign investors. Its proximity to the emerging markets in the Middle

DSM-IV-TR'nin (American Psychiatric Association 2005) kesin taný kriterleri nedeniyle somatizasyon bozukluðu aslýnda seyrek rastlanan bir durumdur; oysa daha hafif bir formu

En son psikiyatrik muayenede; kendine bakým iyi, konuþ- ma açýk, anlaþýlýr, amaca yönelik, duygulaným uy- gun, bilinç açýk, kooperasyon ve yönelim tam, gerçeði

Bu çalışmada, 3D yazıcılar için geliştirilen elyaf takviyeli ince agregalı yüksek performanslı betonun karışım tasarımı ile taze ve sertleşmiş hâlde beton

Bundan önce olduğu gibi bundan sonra da bu kesime enflasyonun üzerin den net gelir sağlamaya çalışacağız, önümüzdeki 5 yıl bunu yapacak vaktimiz de olacak"