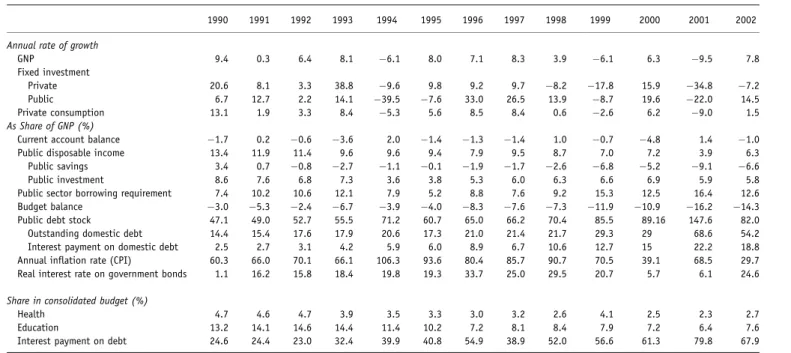

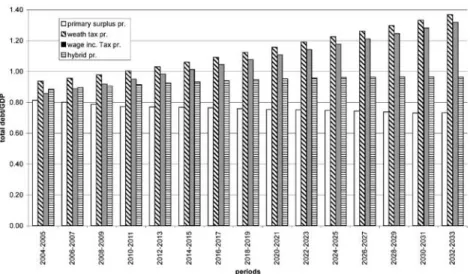

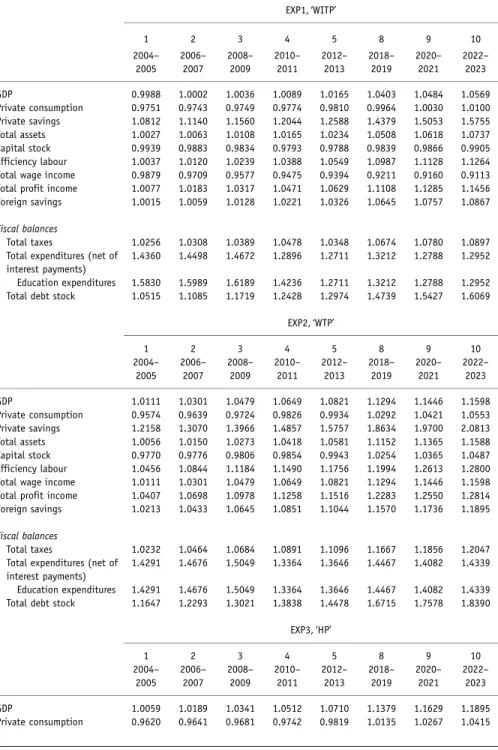

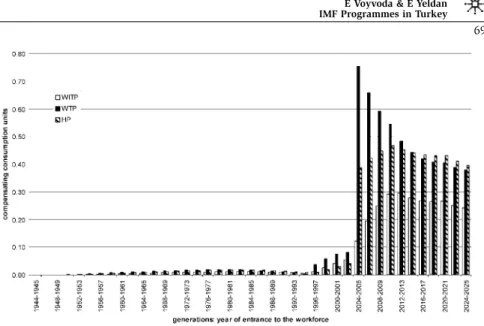

IMF programmes, fiscal policy and growth: investigation of macroeconomic alternatives in an OLG model of growth for Turkey

Tam metin

Şekil

Benzer Belgeler

Sadece genel sa¤l›k alg›lamas› (GSA) de¤erleri yoga grubunda egzersiz grubuna göre daha yüksek bulundu (Tablo 2).Tedavi sonra- s›nda yap›lan de¤erlendirmede, sol ve sa¤

As the algorithms mentioned above, perfect reconstruction of the initial field can also be obtained from the CG based algorithm when the number of given samples are larger than

In this section we investigate an accurate calculation method for transformer ratio, n If we ignore the effect of the negative spring softening capacitance, −C0 , the transformer

In this study, we aimed to produce functional polyvinyl alcohol (PVA) electrospun nanowebs containing essential oil; eugenol (EG), that have long-term durability and

Göktulga’nın, “gelenekçi tipler” olarak çizdiği erkek öykü kişileri, modernleşme sürecinin Türk toplumunda yarattığı “kollektif şizofreni”nin bireysel

This section is divided into three parts, which discuss the importance of design in the resulting self-assembled nanostructures of different classes of peptides, namely

107 年度楓林文學獎決審會與得獎名單,本屆首度增設醫療小說組 107 年臺北醫學大學楓林文學獎,自 10 月 5 日截 止收件後,經過兩輪評審過程,於 11

醫生,請問吃藥配胃藥,正確嗎?