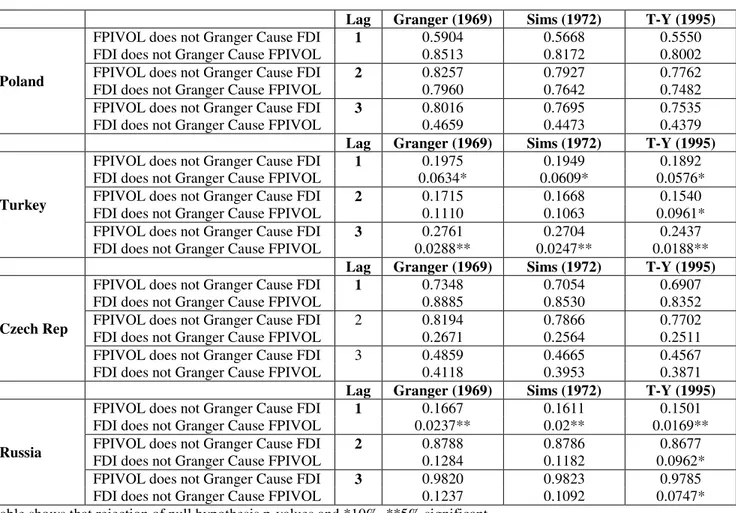

Causality relations between foreign direct investment and portfolio investment volatility

Tam metin

Şekil

Benzer Belgeler

D) the people who made the statues were excellent engineers E) Easter Island is a long way from the nearest continent 38.-40. soruları verilen parçaya göre cevaplayınız.. It is

Lokal komplikasyon gelişen olgular haricinde profilaktik antibiyotik verilmesi tartışmalı olsa da yılan ağız florasında çok çeşitli aerob-anaerob

O anlayış, o konuşuş, o çalışış, o tavır, o eda -ki şarkın Türkiyesiydi, tevekkül gibi görünen isyandı, mah viyet gibi görünen gururdu, sükûnet

3 Şubat 2002'deyse albümdeki bütün sanatçılar, Barış Manço'yu şarkılarıyla anmak için Mydonose Shovvland'de olacak ve sîz leri bekleyecekler.. Ben onu modern

Fakat işini iyi yapan hizmet sağlayıcılarıyla çalıştıkları takdirde lojistik hizmetini ve kendi ana faaliyetleri dışındaki tüm faaliyetleri dış kaynaklardan sağlamak

DSM-IV-TR'nin (American Psychiatric Association 2005) kesin taný kriterleri nedeniyle somatizasyon bozukluðu aslýnda seyrek rastlanan bir durumdur; oysa daha hafif bir formu

En son psikiyatrik muayenede; kendine bakým iyi, konuþ- ma açýk, anlaþýlýr, amaca yönelik, duygulaným uy- gun, bilinç açýk, kooperasyon ve yönelim tam, gerçeði

Bu süre içinde ilki Orhan Günşiray’la, İkincisi Recep Bilginer’le ortak olmak üzere iki kez film yapımcılığını da denedi?. “ Selvi Boylum Al