Monatery Policy and Financial Market in Kuwait and Algeria

Tam metin

Şekil

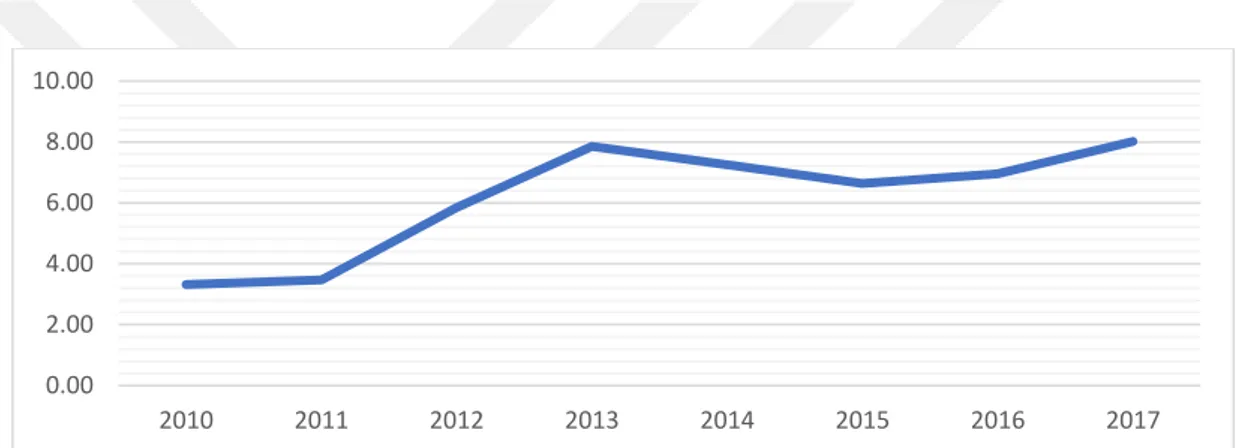

![Figure 2.10 Growth Rates of Local Liquidity in the Arab Countries for 2016 and 2017 [60]](https://thumb-eu.123doks.com/thumbv2/9libnet/3389789.12818/61.892.168.785.121.411/figure-growth-rates-local-liquidity-arab-countries.webp)

![Figure 3.2 Hydrocarbons Revenues and Non- Hydrocarbons Revenues during the period 2000-2015 (Billion of the Dinar) [74, 75]](https://thumb-eu.123doks.com/thumbv2/9libnet/3389789.12818/70.892.157.807.278.618/figure-hydrocarbons-revenues-hydrocarbons-revenues-period-billion-dinar.webp)

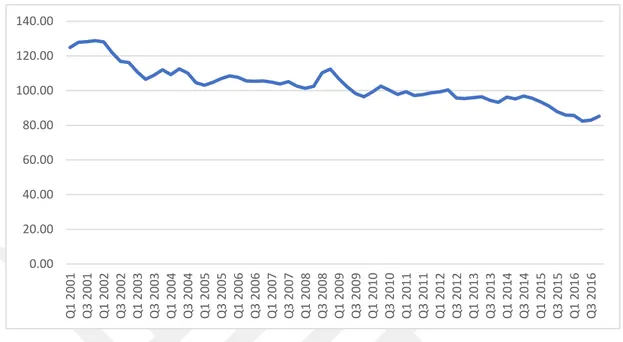

![Figure 3.4 Relationship between Foreign Exchange Reserves and Oil Price during 2000- 2000-2016 [78]](https://thumb-eu.123doks.com/thumbv2/9libnet/3389789.12818/72.892.155.786.127.528/figure-relationship-foreign-exchange-reserves-oil-price.webp)

![Figure 3.7 The Difference between Actual and Target Inflation Rate in Algeria [84, 85]](https://thumb-eu.123doks.com/thumbv2/9libnet/3389789.12818/77.892.159.781.124.493/figure-difference-actual-target-inflation-rate-algeria.webp)

Benzer Belgeler

Yunanistan’ın Anadolu’yu terk edeceğine dair söylentilerin ortaya çıkması üzerine tarih sahnesinde yerini almış olan Helen Anadolu Savunma [Mikrasiatiki

Bulguların yorumlanması: Bu basamaklar: (i) Sayma basamağı, verilerin bilişsel kurgu gruplarına ayrıştırılması ve kategorilerde yer alan frekansların ölçülmesi;

Bu çalışmanın yapılmasındaki amaç, Türkiye’de 2006 yılında kurulmaya başlayan Bölgesel Kalkınma Ajanslarının bölgesel düzeyde yapmak istedikleri projelere,

We generate the random potential using an optical speckle pattern, whose induced forces act strongly on one species of particles (strong particles) and weakly on the other

透過連線測試以及視訊畫面品質測試的結果,可 以清楚了解到:無論用無線移動式裝置透過 3.5G、或 WLAN 連結視訊照護系統,還是以有線的 LAN

Being motivated with the fact that, the data were enough to model private manufacturing sector price index for the pre-crisis sample period, in this thesis, we

Buna karşılık Türk şiirini ve şairler ni hiç bilmiyor ve takip elmiyordı Onun neredeyse bir duvar gibi sağır kal dığı yerli şiirimiz o sıralar "Garip

İlmî heyetin tasarısı seçimlerde işlenecek kanunsuz hareketlere ağır ceza vermek ve suçların takibini serî bir muhakeme usulüne tâbi tutmak ve suçluların bir