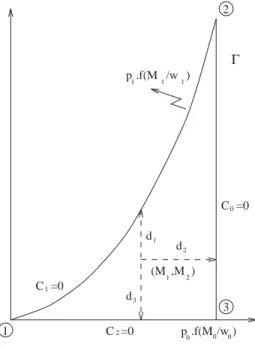

Existence of competitive equilibrium under financial constraints and increasing returns

Tam metin

Şekil

Benzer Belgeler

One alternative approach, the entrapment of enzymes in conducting polymer matrices during electrochemical polymerization, is attracting great interest, because it

On the other hand, modification tuples of virtual classes do not contain update information because updates are solely performed against base classes in our

It has been believed that the temperature generally has two major effects on the adsorption process. Increasing the temperature will increase the rate of diffusion of the

Measured absorption of the GaAs film (Figure S1), one- dimensional spectra, obtained in the scattering and lasing experiments (Figure S2), and the Q factor and near- field analysis of

Figure 5.2: Time series graphs of Yapi Kredi Bank and Vakıfbank stock prices Table 5.1 presents the Johansen Cointegration Test output for the pair Akbank-Fortis. The

The so-called Additamenta to the Book of Armagh record that Áed visited Armagh during the episcopacy of Ségéne (r. 661–88) in order to incorporate Sletty into the Patrician

Politics may be separate from ruling and being ruled (according to Arendt), may be supportive of ruling and being ruled (according to Oakeshott, Collingwood and Schmitt), and may

For the problem with the objectives of minimizing total cost and maximum match-up time, we get the initial job pool by solving the MM problem and setting the match-up time on