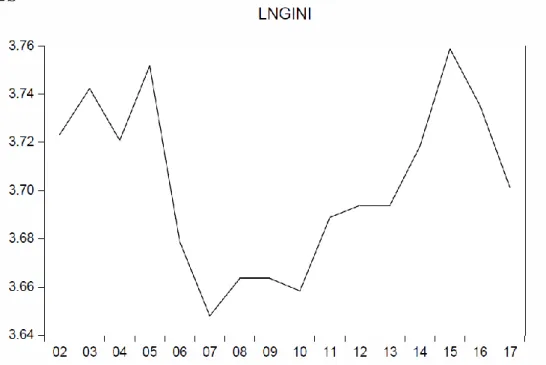

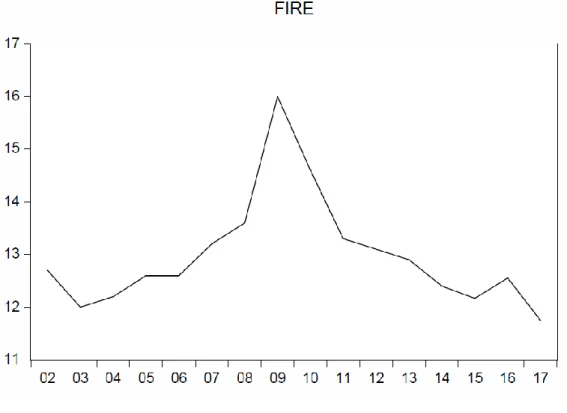

Effects of financialization to income inequality in Turkey

Tam metin

Şekil

Benzer Belgeler

Accordance with the empirical results, our study concluded that, Return on Assets and Credit Risk of the banks in Central Asian countries don’t have significant impact on

[r]

Türkiye Dış İşleri Vekâleti Umumî Kâtibi Cevat Açıkalın, Amerika Büyük Elçimiz Selim Sarper, Birleşmiş M il letler Genel Sekreteri Dag Hanimarskjold ve

Bununla beraber, o vakte kadar muhafaza ettiği bir saygı ve edep duygusu artık maziye karışıyor, di ğer bir tarifle yüzünden indirme, diği.. dirayet yahut

Poliakoff, Archipenko, Hartung ve Zadkine gibi Paris Ekolü'nün önde gelen sanatçıla rıyla birlikte sergiler açan Anlı'nın eserlerinin bulunduğu müzeler şunlar:

Made of multi-layers of cotton, silk or wool, the tents are usually plain on the outside, the walls lavishly decorated with intricate applique and embroidery on the

E rtuğrul Soysal ortaokulda i- ken babasım n h ed iye ettiği akor deon ile tango çalm aya başlamış. A n ka ra’da M ülkiye’de okurken konservatuvara da devam edip no

Every year, tens of thousands of people risk their lives trying to enter the EU in an irregular way and many die in the attempt, as demonstrated by recent events, notably in