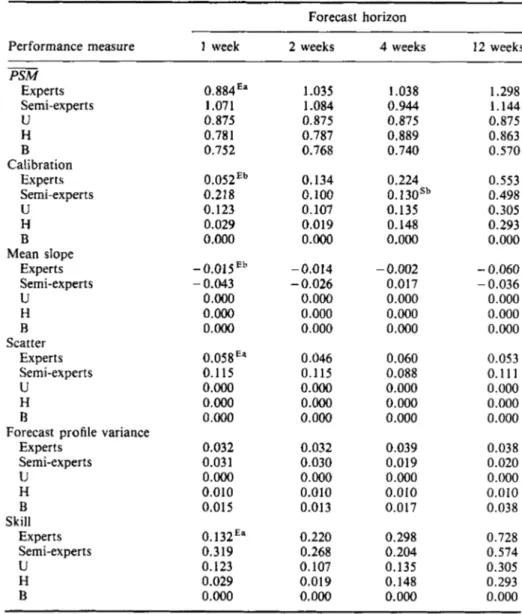

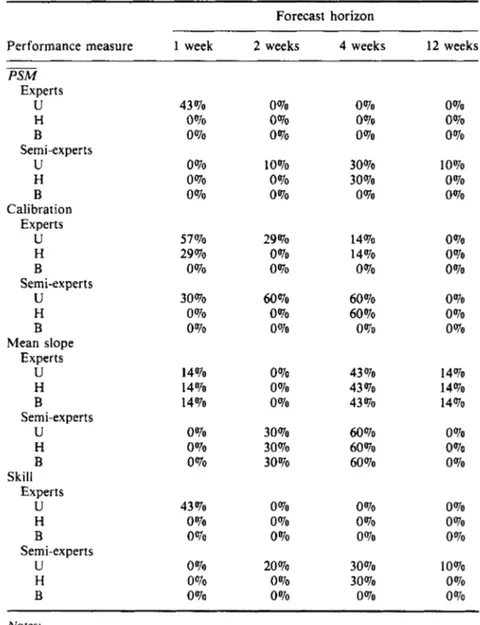

An exploratory analysis of portfolio managers' probabilistic forecasts of stock prices

Tam metin

Şekil

Benzer Belgeler

The basic idea of optical waveguides is to confine and propagate light in dielectrics or semiconductors, as opposed to free space opticsT^ 'fliis can be managed b,y

Fransız çocuk edebiyatı Anglosakson çocuk edebiyatının yanında saygı değer bir yer tutabilmişse, daha çok Jules Verne sayesinde olmuştur bu.. Yüzbir cild

Ahmet Mithat’ın “Çingene” Adlı Romanında Ötekine Duyulan Arzu Üzerine Bir

R: right; L: left; Gr: channels that show group difference in 2 £ 2 (Group £ Hand) repeated measures ANOVA results; AG: angular gyrus; SPG: superior parietal gyrus; SMG:

Âdile sultanın zevcine tartı muhabbeti rıhtımdaki saat hâdise siyle başlamıştır ve Mehmet AU paşa ölünceye kadar sultan kocasına rûm t olmuştur.. Sonra

Bulgaristan’daki Bektaşi türbelerden en iyi bilinen ve aktif olarak işlevini sürdüren türbeler Demir Baba (Kuzey Bulgaristan’da Isperih’in yakınında), Teketo’daki Otman

Pretreatment with levosimendan provided better protection in our study groups, especially under moderate hypothermic (28 °C) conditions, compared with IP with

✔ Aim: Anaplastic ganglioglioma is a rarely seen, high grade malignant glial neoplasm comprising of neoplastic ganglion cells Since gangliogliomas with an anaplastic