Foreign direct investment in Turkey and Latin American countries: a comparative perspective, 1980-1995

Tam metin

Şekil

Benzer Belgeler

Bugün iz leyeceğimiz bölümde Sanayi-i Ne fise Mektebi 'nin resim atölyeleri nin Türk öğretmenlerin sorumlu luğuna geçmesi, Türk resim tari hine 1914 Kuşağı ya

O anlayış, o konuşuş, o çalışış, o tavır, o eda -ki şarkın Türkiyesiydi, tevekkül gibi görünen isyandı, mah viyet gibi görünen gururdu, sükûnet

DSM-IV-TR'nin (American Psychiatric Association 2005) kesin taný kriterleri nedeniyle somatizasyon bozukluðu aslýnda seyrek rastlanan bir durumdur; oysa daha hafif bir formu

En son psikiyatrik muayenede; kendine bakým iyi, konuþ- ma açýk, anlaþýlýr, amaca yönelik, duygulaným uy- gun, bilinç açýk, kooperasyon ve yönelim tam, gerçeði

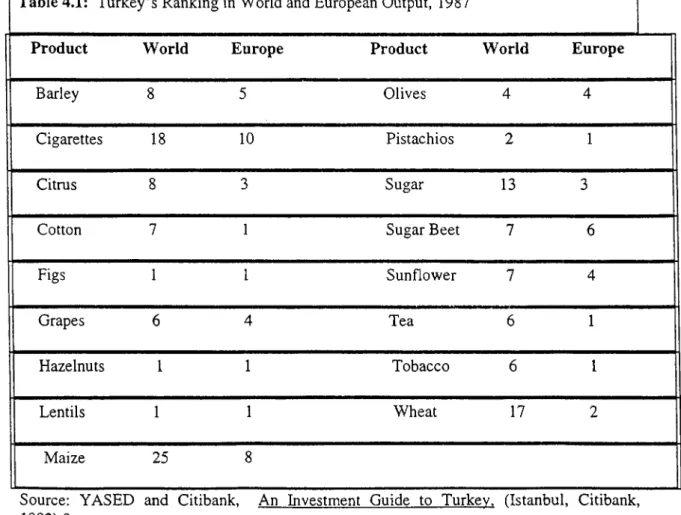

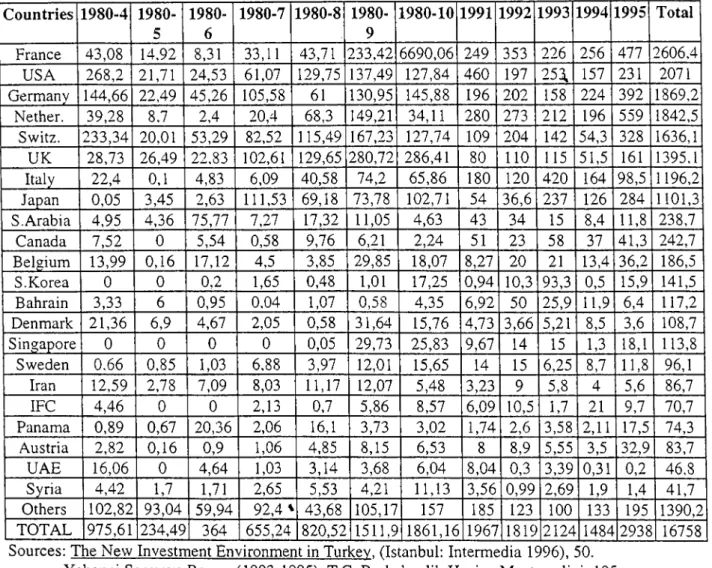

In his research, Bosut (1999) describes Turkey as a large and growing domestic market for the foreign investors. Its proximity to the emerging markets in the Middle

On the other hand, it is possible to provide fast and yet successful approximations to solutions of such partitioned matrix systems using Schur complement reduction...

Main results In this section, we give an interval-valued right-sided Riemann–Liouville fractional integral of a function F and then we prove the Hermite-Hadamard inequality for

Lokal komplikasyon gelişen olgular haricinde profilaktik antibiyotik verilmesi tartışmalı olsa da yılan ağız florasında çok çeşitli aerob-anaerob