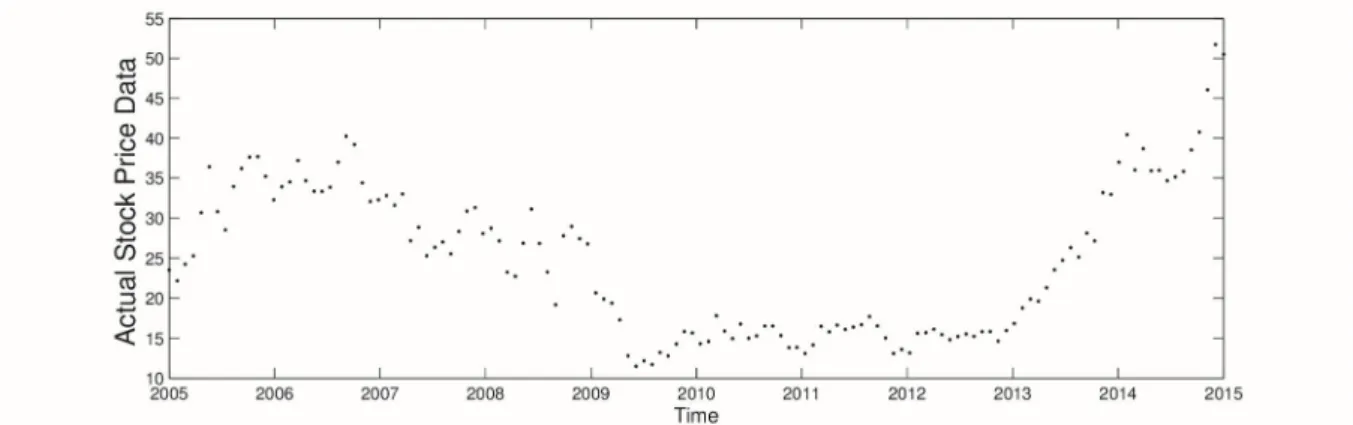

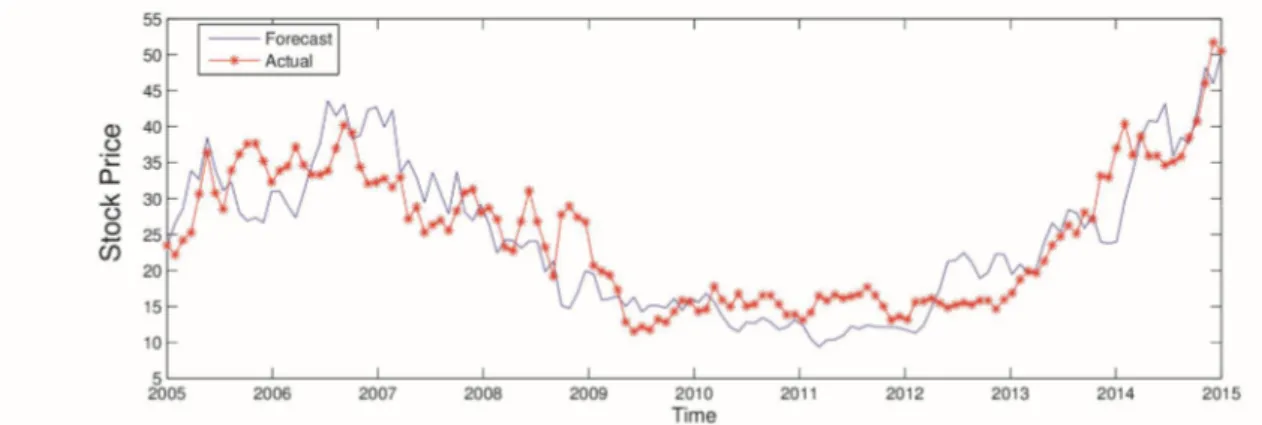

Parameter Estimation an a Black Scholes

Tam metin

Şekil

Benzer Belgeler

In our study, it was aimed to investigate allergen sensitivities, especially house dust mite sensitivity in pre-school children with allergic disease complaints by skin prick

This study aims to examine EFL learners’ perceptions of Facebook as an interaction, communication, socialization and education environment, harmful effects of Facebook, a language

With the reduction of indium composition from the pure InAs case, the in-plane and biaxial strain diminishes as well as the quadrupolar energy splitting, whereas the increased

of Provincial Directors of Youth Services and Sports concerning the education and political sub- dimension in terms of the place of duty variable don’t differ in a way that can

The mathematical representation of the conceptual model for the case study is a multi-objective mixed-integer model that con- siders transporting hazardous wastes and siting

However, before the I(m)Press, my other project ideas were not actually corresponding to typography. Therefore, I received a suggestion to make an artist’s book with an efficient

Since the historically observed average real interest rate on Turkish T-Bills is 14.12 percent and the average real stock returns is 9.84 percent, observed equity premium in

In the case of Mexico, for example, the authors argue that the inflation targeting regime has allowed for more flexible monetary policy than had occurred under regimes with