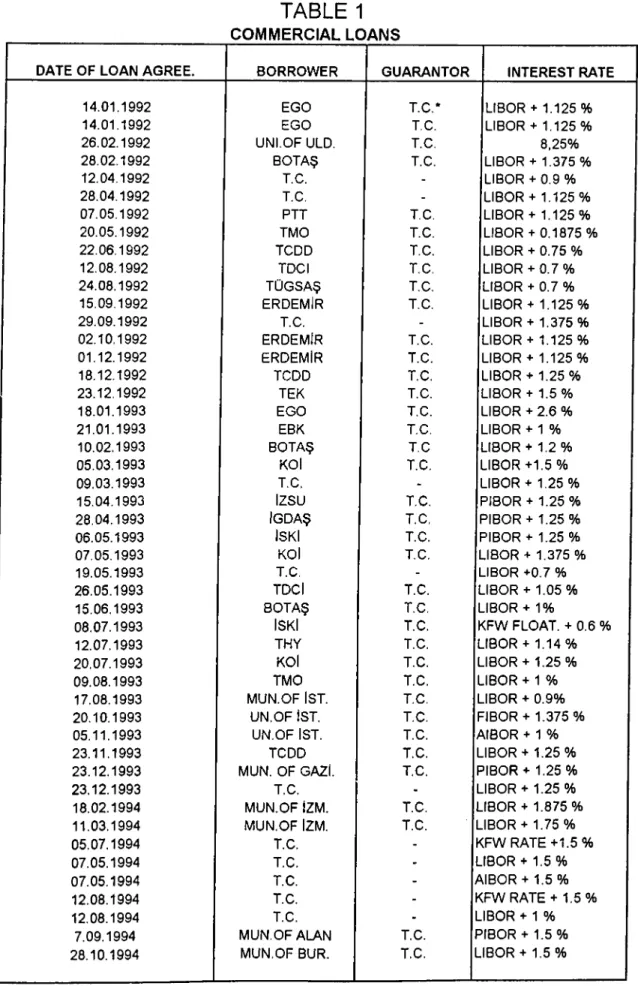

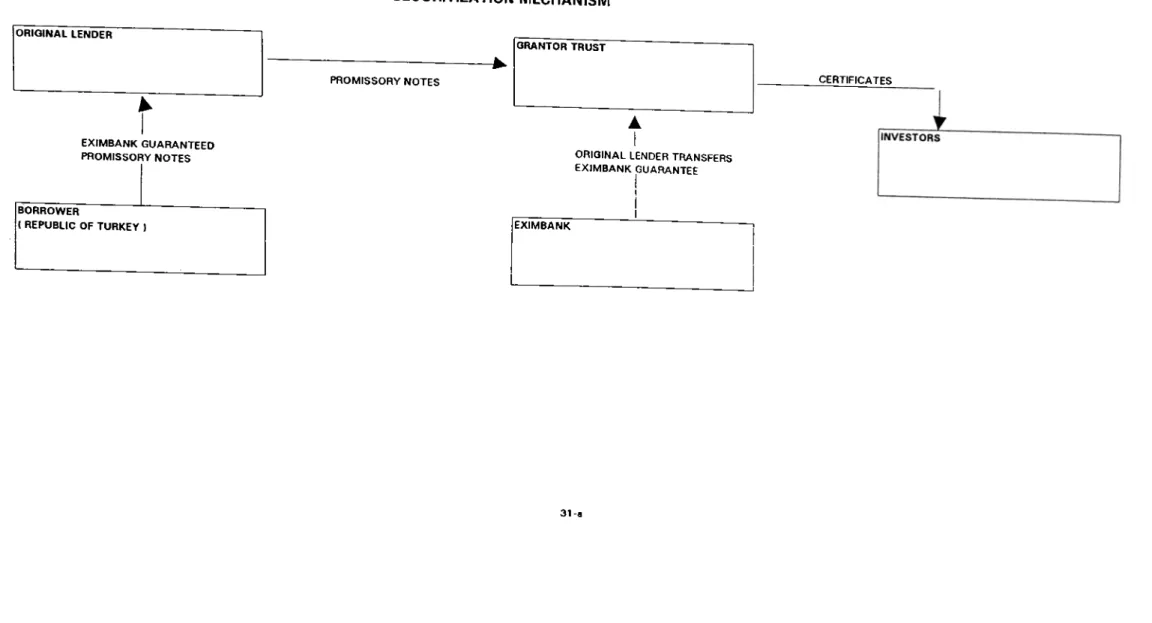

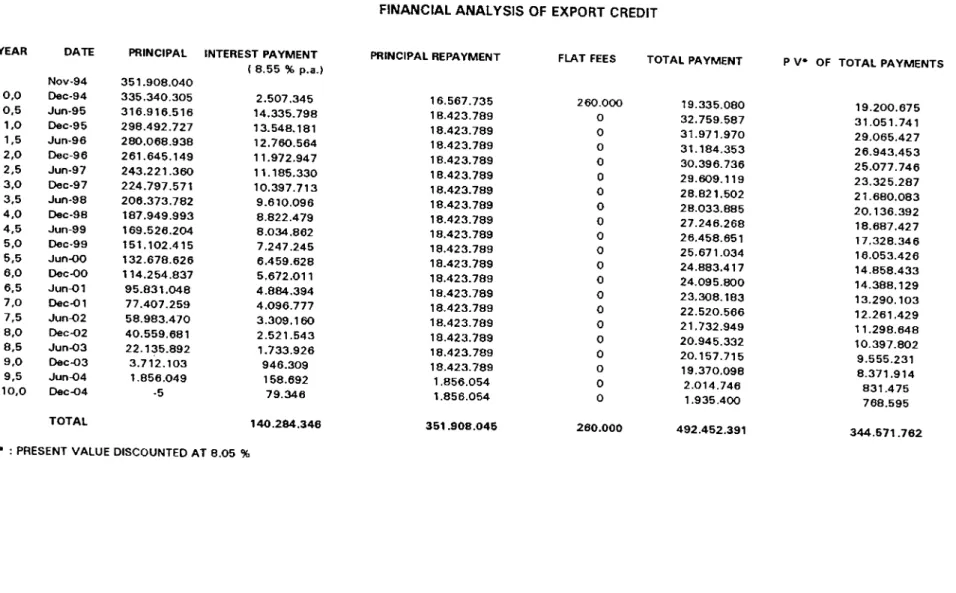

Analysis of securitization of an export credit in Turkey

Tam metin

Şekil

Benzer Belgeler

Bunu bir örnekle açıklayalım: Kaçırılan, araba kazası geçiren ya· da cinsel saldırıya uğrayan bir çocuk, çeşitli korkular ve bunalımlar geliştirir.

İnsanın vejetaryen olduğuna dair görüş ve kanıt bildirilirken en büyük yanılma biyolojik sınıflandırma bilimi (taxonomy) ile beslenme tipine göre yapılan

Göllerin, istek üzerine süresi uzatılacak şekilde, 15 yıllığına özel şirketlere kiralanacağı belirtiliyor.Burada "göl geliştirme" adı verilen faaliyet,

l~yların sakinleşmesine ramen yine de evden pek fazla çıkmak 1emiyorduk. 1974'de Rumlar tarafından esir alındık. Bütün köyde aşayanları camiye topladılar. Daha sonra

,ldy"ryon ordı, ırnığ rd.n ölcüm cihazlan uy.nş ü.rinc. saİıtrd fıatiycılcri

The relevant data and evidences were gathered from the writings of Vinoba, the writings of others, on the educational thought of Vinoba, and visitation to Vinoba's and Gandhi's

Erzincan'ın İliç ilçesinin çöpler köyünde altın çıkarmaya hazırlanan çokuluslu şirketin, dönemin AKP'li milletvekillerini, yerel yöneticileri ve köylüleri gruplar

Öte yandan, hemen her konuda "bize benzeyeceksiniz" diyen AB'nin, kendi kentlerinde yüz vermedikleri imar yolsuzluklar ını bizle müzakere bile etmemesi; hemen tüm