Determinants of investment in the manufacturing sector in Turkey

Tam metin

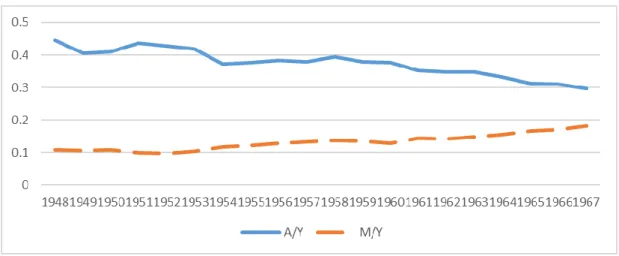

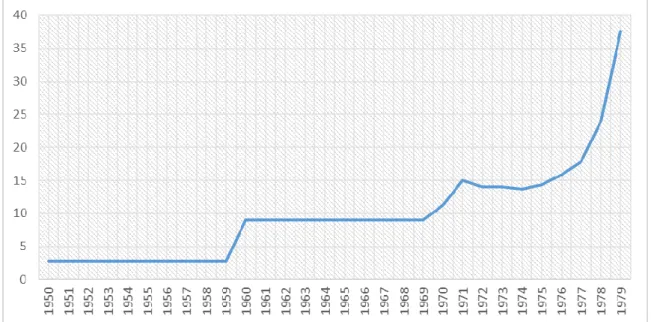

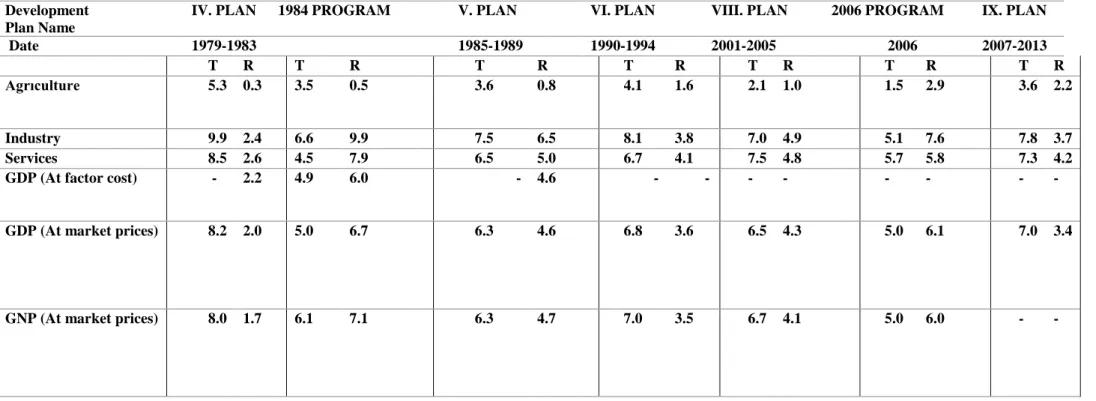

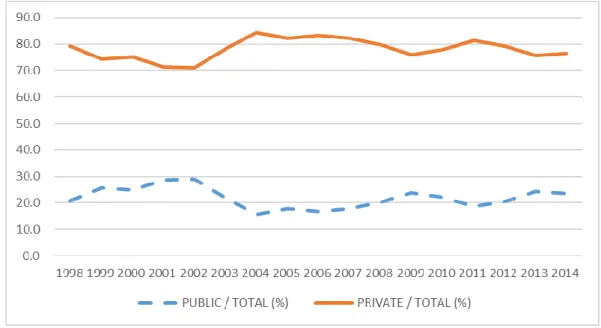

Şekil

Benzer Belgeler

Bu çalışmada, 3D yazıcılar için geliştirilen elyaf takviyeli ince agregalı yüksek performanslı betonun karışım tasarımı ile taze ve sertleşmiş hâlde beton

Bu arada 12 Eylül roman ve anılan (aniden ve nedense şimdi) birer birer (Osman Akınhayın romanı, Tank Akan ve Gün Zileli nin anılan) sökün etm eye başlamışken,

This is because there is an increase in economic performance is causing positive changes in bank performance and this suggests that the improvement in

The foreign investments was affecting Jordan in a positive way, but recently the situation changed, and this type of investments started to affected the Jordanian economy in

The indigenous parameters include general firm characteristics (such as firm’s age, size, ownership status etc.), intellectual capital (human capital, social

Currently, local private equity (PE) funds—backed up by international development finance institutions (DFIs) and local banks channelling programmed loans from DFIs to local firms

In his research, Bosut (1999) describes Turkey as a large and growing domestic market for the foreign investors. Its proximity to the emerging markets in the Middle

When shaping their strategies, policies, and plans for the near future, they have specified consistent quality level as the top competitive priority, increasing