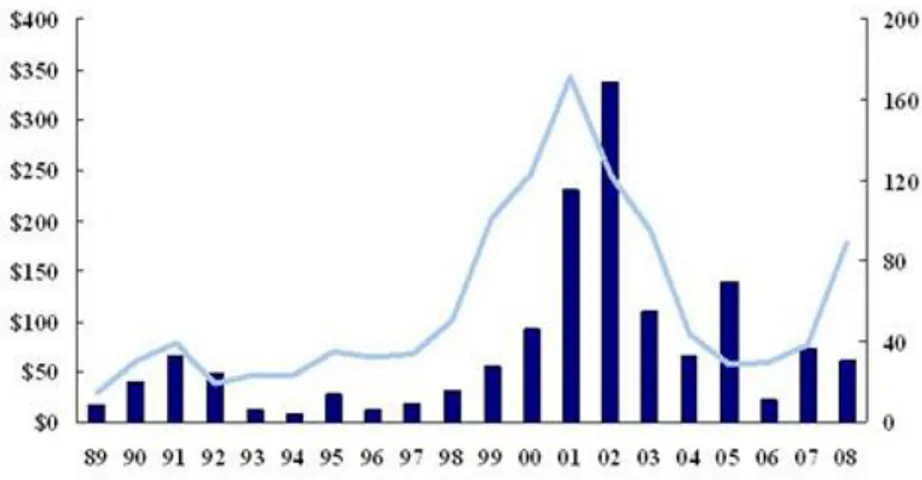

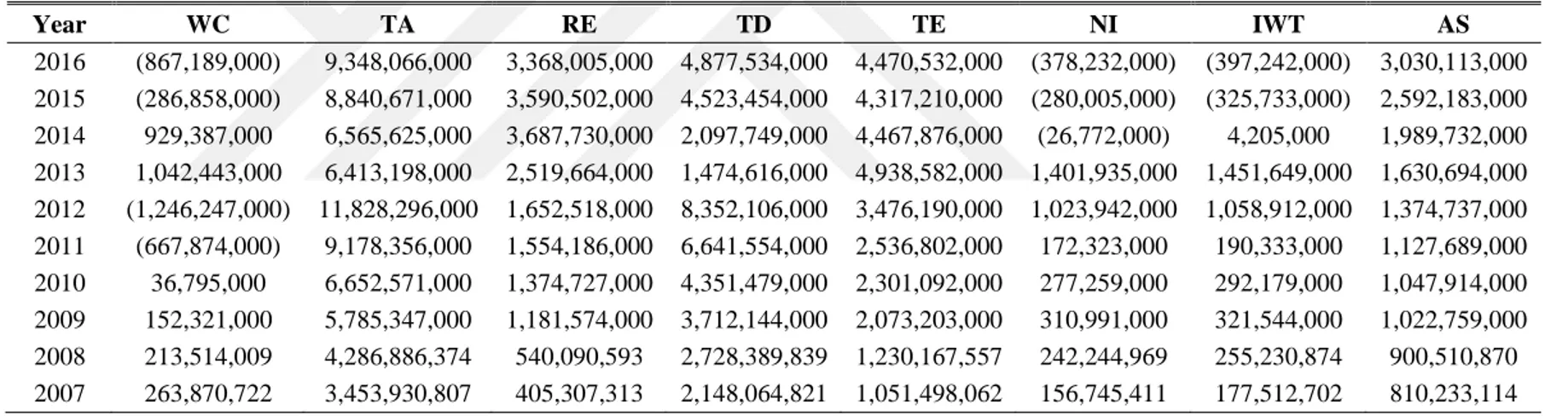

ESTIMATING THE PROBABILITY OF BANKRUPTCY USING Z-SCORE AND DISTANCE TO DEFAULT MODEL: AN APPLICATION ON ISE

Tam metin

Şekil

Benzer Belgeler

It is seen that the perovskite phase is highest in the sample annealed at 750 °C indicating that a relatively high temperature is necessary for complete transition of PMNT to

enhancement in plasmonic SM device results from light scattering and LSPR effect rather than the morphology change of the SM BHJ layer induced by Au-silica

Elde edilen taşkın yayılım haritaları üzerinde yapılan değerlendirmeye göre; özellikle 100 yıl ve daha büyük tekerrür süreli taşkınlarda Bingöl İl merkezindeki

Bu çalışmanın amacı sodyum hidroksit (NaOH) ve potasyum hidroksit (KOH) katalizörleriyle üretilen kanola biyodizelinin üretimi esnasında katalizör miktarı ve

Bu nedenle, politika transferleri, ya- bancı uzmanlardan yararlanma ve alınan askeri yardımlar bakımından büyük benzerlikler taşıyan ve zamansal olarak 1700-2016

Keywords : Speech coding, lineiir predictive coding, vocal tract parameters, pitch, code excited linear prediction, line spectrum

The Cesaro summability of trigonometric Fourier series is investigated in the weighted Lebesgue spaces in a two-weight case, for one and two dimensions.. These results are ap- plied

Halkla ilişkiler uygulamacıları, sosyal sorumluluk düşüncesi ile paralellik gösteren bir biçimde etik açıdan kime sadakat gösterecekleri konusunda iki seçeneğe