F Ö !? £ C ^ S T !H G Т Щ F Q » £ i S ä

G ü S S E H C Y P R I S E S t iS lla S

g ШШ і Ш Ш

8

à P P s S â â S i

i“ ί Гл ! |j 11J »i *5i» w4 1? W ж ^ .üt

1·()ΚΚΓΛ8ΐ1Ν<; THK FÜliKKiN CIİRKKNCV H R K 'K S IJSIN(; ΓΙΙΕ BOX JE N K IN S APPROACH

A THESIS

SUBMITTED TO THE DEPARTMENT OF MANAGEMENT AND THE GRADUATE SCHOOL OF BUSINESS ADMINISTRATION

OF BILKENT UNIVERSITY

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

By

BELGİN İNAN June, I9B‘J

f I О ^

K G -г»

in i

H TSCf® і е б

5

I certify that I have read this thesis and that in my opinion it

is fully adequate, in scope and quality, as a thesis for the

degree of Master of Business Administration.

Assist. Prof. Dilek Yeldan

I certify that I have read this thesis and that in my opinion it

is fully adequate, in scope and quality, as a thesis for the

degree of Master of Business Administration.

Assist. Prof. Kürsat AydoQan

I certify that I have read this thesis and that in my opinion it

is fully adequate, in scope and quality, as a thesis for the

degree of Master of Business Administration.

Assist. Prof. Erdal Erel

Approved for the Graduate School of Business Administration

Prof. Dr. Subidey Togan

ACKNOWLEDGEMENT

I wish to thank Dr. Dilek Yeldan, Dr. Kursat AydoQan, and Dr.

Erdal Erel for their advice, guidance, and encouragement

throughout the course of this thesis.

ABSTRACT

FORECAST [NT. ΓΙΙΚ l-ORKiGN CURRENCY P R IC E S USING THE BOX JE N K I N S APPROACH

İnan M.B.A. in Management

Supervisor: Assist. Prof. Dilek Yeldan June 1989, 96 pages

In this thesis, the Box Jenkins approach is applied to forecast the future prices of foreign currencies, American Dollar and

German Mark, in Turkey’s Black Market using available

observations made between the years 1985-1988. The forecasts obtained from this approach are compared to the real available observations. The results show that the Box Jenkins approach is not accurate enough in this case because of the large mean absolute deviation between the forecasted and the observed values of these currencies due to the significant residuals generated in the diagnostic checking stage.

Ki-yworils; E’orecast:ing. Box Jenkins, foreign currency

OZIvT

BOX JKNKINS MKTÜDUNÜ KULLANARAK DÖVİZ FİYATLARININ TAHMİNİ

Belidin İnan

İs İdaresi Yüksek Lisans

Denetçi: Yrd. Doç. Dr. Dilek Yeldan Haziran 1989, 96 sayfa

Bu tezde Box Jenkins metodu ile Türkiye’de serbest piyasadaki Amerikan Doları’nın ve Alman Markı’nın değerleri, 1985-1988

yılları arasındaki gerçek değerler kullanılarak tahmin

edilmiştir. Elde edilen öngörüler gerçek değerlerle

karş1laştır1Imıştir. Teşhis kontrol aşamasında ortaya çıkan

anlamlı artıklara bağlı olarak, öngörülen sonuçlar ve gerçek sonuçlar arasındaki ortalama mutlak sapmaların büyüklüğü nedeni

ile, Box Jenkins metodunun verdiği sonuçların yeterli derecede doğru olmadığı gösterilmiştir.

CHAPTER 1- INTRODUCTION ... 1

1.1. Problem Definition ... 1

CHAPTER 2- FORECASTING METHODS ... 2

2.1. Introduction ... 2

2.2. Forecasting techniques 4 2.3. Box Jenkins method of forecasting ... 12

2.4. Common ARIMA processes ... 16

CHAPTER 3- APPLICATION OF BOX JENKINS METHOD USING AMERICAN DOLLAR ... 18

3.1. Identification ... 1*?

3.2. Estimation ... 21

3.3. Diagnostic checking ... 22

3.4. Forecasting ... 24

CHAPTER 4- APPLICATION OF BOX JENKINS METHOD USING GERMAN MARK ... 29

4.1. Identification ... 29

4.2. Estimation ... 30

4.3. Diagnostic checking ... 30

4.4. Forecasting ... 31

CHAPTER 5- RESULTS & CONCLUSIONS ... 35

REFERENCES ... 38 APPENDIX A- FIGURES ... 41 APPENDIX B- TABLES 78 TABLE OF CONTENTS Subject Page No V I

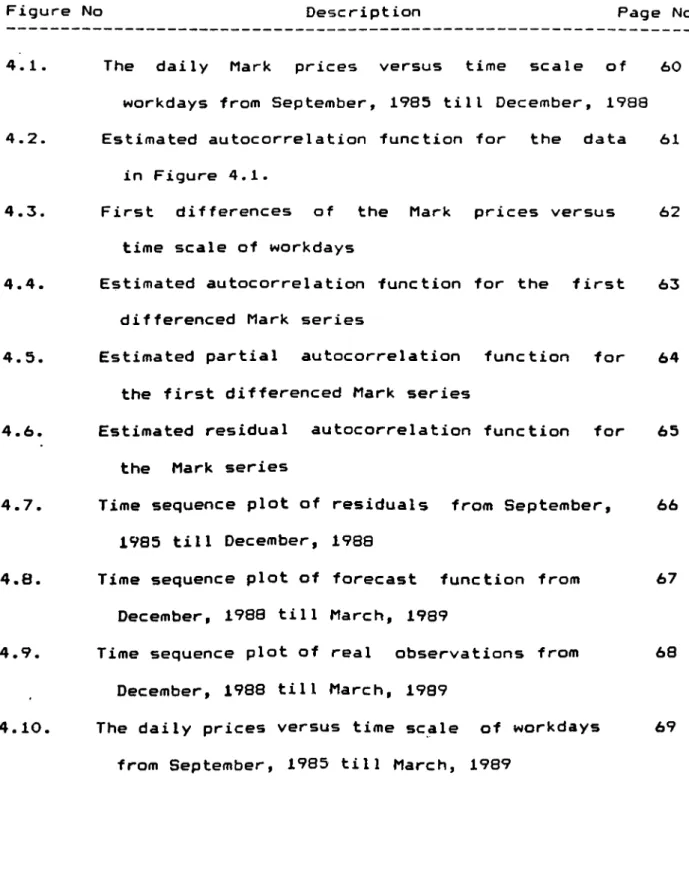

LIST OF FIGURES

Figure No Description Page No

3.1. The daily Dollar prices versus time in workdays 42

from September, 1985 till December, 1988

3.2. Estimated autocorrelation function for the 43

Dollar series

3.3. First differences of the Dollar values versus 44

time in workdays

3.4. Estimated autocorrelation function for the 45

first differenced Dollar series

3.5. Estimated partial autocorrelation function for 46

the first differenced Dollar series

3.6i Estimated residual autocorrelation function 47

for the Dollar series

3.7. Time sequence plot of residuals for Dollar 48

series for the years September, 1985 till

December, 1988

3.8. Time sequence plot of forecast function for 49

December, 1988 till March, 1989

3.9. Time sequence plot of real observations for 50

December, 1988 till March, 1989

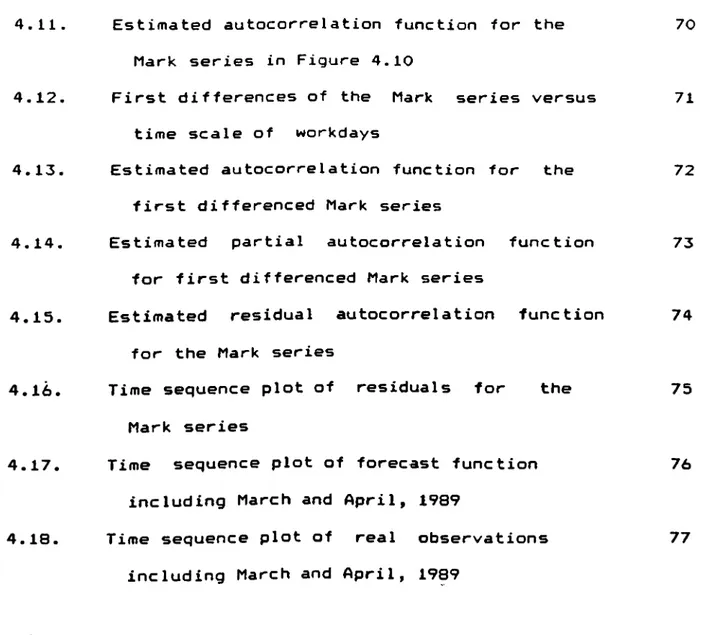

LIST OF FIGURES CONTINUED

Figure No Description Page No

3.10 The daily Dollar prices versus time scale of 51

workdays from September, 1985 till March, 1989

3.11. First differences of the daily Dollar prices 52

of Figure 3.10

3.12. Estimated autocorrelation function for the 53

first differenced Dollar series

3.13. Estimated partial autocorrelations for the first 54

differenced Dollar series

3.14. Estimated residual autocorrelation function 55

for the Dollar series

3.15. Time sequence plot of the forecast function 56

for March and April, 1989

3.16. Time sequence plot of residuals for the years 57

September, 1985 till March, 1989

3.17. Time sequence plot of forecast function for the 58

second differenced Dollar series for March and April, 1989, model AR(2)

3.18. Time sequence plot of forecast function for 59

the first differenced Dollar series for March

and April, 1989, model AR(2), MA(1)

LIST OF FIGURES CONTINUED

Figure No Description Page No

4.1. The daily Mark prices versus time scale of 60

workdays from September, 1985 till December, 1988

4.2. Estimated autocorrelation function for the data 61

in Figure 4.1.

4.3. First differences of the Mark prices versus 62

time scale of workdays

4.4. Estimated autocorrelation function for the first 63

differenced Mark series

4.5. Estimated partial autocorrelation function for 64

the first differenced Mark series

4.6. Estimated residual autocorrelation function for 65

the Mark series

4.7. Time sequence plot of residuals from September, 66

1985 till December, 1988

4.0. Time sequence plot of forecast function from 67

December, 1988 till March, 1989

4.9. Time sequence plot of real observations from 68

December, 1988 till March, 1989

4.10. The daily prices versus time scale of workdays 69

LIST OF FIGURES CONTINUED

Figure No Description Page No

4.11. Estimated autocorrelation function for the

Mark series in Figure 4.10

4.12. First differences of the Mark series versus

time scale of workdays

4.13. Estimated autocorrelation function for the

first differenced Mark series

4.14. Estimated partial autocorrelation function

for first differenced Mark series

4.15. Estimated residual autocorrelation function

for the Mark series

4.16. Time sequence plot of residuals for the

Mark series

4.17. Time sequence plot of forecast function

including March and April, 1989

4.18. Time sequence plot of real observations

including March and April, 1989

70 71 72 73 74 75 76 77

LIST OF TABLES

Table No Description Page No

3.1. Summary statistics for the Dollar series 79

including September, 1985 till December, 1988

3.2. Summary statistics for the first 80

differenced Dollar series

3.3. Summary of estimation stage values for 81

the Dollar series

3.4. Forecast values with their lower and 82

upper limits for Dollar series from December, 1988 till March, 1989

3.5. Summary statistics for the Dollar series 83

including September, 1985 till March, 1989

3.6. Summary statistics for the first 84

differenced Dollar series

3.7. Summary of estimation stage values for 85

the Dollar series for period, September, 1985 till March, 1989

3.8. Forecast values with their lower and 86

upper limits for Dollar series including March and April* 1989

LIST OF TABLES CONTINUED

Table No Description Page No

v5.9. Summary of estimation stage values for 87

the second differenced Dollar series

3.10. Summary of estimation stage values for 08

the model AR(2), MA(1)

4.1. Summary statistics for the Mark series 89

including September, 1985 till December, 1980

4.2. Summary statistics for the first 90

differenced Mark series

4.3. Summary of estimation stage values for 91

the Mark series

4.4. Forecast values with their lower and 92

upper limits for the Mark series

4.5. Summary statistics for the Mark series 93

including September, 1985 till March, 1989

4.6. Summary statistics for the first 94

differenced Mark series from September,

1985 till March, 1989

4.7. Summary of estimation stage values for the 95

Mark series including September, 1985 till March, 1909

4.0. Forecast values with their lower and upper 96

limits including March and April, 1989

CHAPTER 1

INTRODUCTION

1.1. P r o b l e m DefinitionRecent economic policies of C e ntral B ank in Turkey have had a

d r a s t i c impact on the Black Market pr i c es of foreign currencies and make s one wonder about the c h anges that are to occur in these

pric e s in the near future. Many news agencies have been ma king

s p e c u l a t i o n s about the future prices of foreign currencies based on the historical and current data.

Bef o r e A u g u s t 1988, Turkey's C e n t r a l B ank used to set the prices

of the foreign currencies w i thout taking into a ccount the

c o n d i t i o n s of the foreign exchange market in Turkey. This

p o l i c y produced a considerable d i f f e r e n c e between the prices

of the C e n t r a l Bank relative to the p r i c e s of the B l a c k Market. The fo reign exchange rates in the B l a c k Market turned out to be

chea p e r than the prices of the C e n t r a l Bank and for this

reason, m a n y investors and b u s i n e s s m e n preferred to b uy

foreign exchange from the Black M a r k e t rather than the C e n tral

Bank. As a result of this, the C e n t r a l Bank did v ery limited

b u s i n e s s related with foreign e x c h a n g e causing inefficient use

of the fo reign exchange market. S t a r t i n g August 1988, however,

the C e n t r a l B ank changed their p o l i c y by es tablishing new

d i v i s i o n s such as foreign excha n g e and effective exchange

mar k e t s in their body. This allowed the Central Bank to get a

b et t e r c o ntrol of the foreign e x c h a n g e prices in the Black

The Central Bank did not directly intervene the Black Market

in determining the prices of foreign currency, but rather

took some steps that affected these prices in the Black

Market. For example, the government made 57. devaluation in

1986, which resulted in an increase in the prices of foreign

currency in the Black Market, closing the gap between the prices

of foreign currency in the Black Market relative to the

Central Bank. This allows the government to make more

efficient use of foreign currency deposits of the Central Bank

in Turkey. In addition, another factor that could play

a key role for more efficient usage of foreign currency

deposits is to be able to forecast variations in these prices in

the future.

Because Turkey's outside loans are in the form of

Dollars, forecasting the prices of the foreign currency is

very important for Turkey. Some increase in the price of Dollar

can cause a large deficit of Turkey's Treasury and create major

economic problems. For this reason, forecasting the future

prices of foreign currency is important in controlling

the treasury of Turkish Government. Besides, foreign currency

prices affect the investors, especially those who are

importing foreign machines and raw material. By making proper

forecasting, they can control their budget more efficiently and

In this thesis, first, a brief summary on different forecasting

techniques is introduced in Chapter 2. This is followed by

the Box Jenkins method of forecasting that is applied to

project Turkey's Black Market prices of American

Dollar and German Mark for the period December, 1988 and January

and February, 1909 in Chapters 3 and 4. Then, same forecasts

are updated for the period March and April, 1989.

In Chapter 5, these forecast values obtained are then compared

with the real available data for the same time periods in terms

of mean absolute deviation of these two sets, namely the

forecasts and the observations. In addition, the accuracy of the

Box Jenkins approach is discussed based on the above comparisons and the accuracy of the available data.

CHAPTER 2 FORECASTING METHODS

2.1 Introduction

There is frequently a time lag between the realization that an

event is going to happen and the occurrence of that event. This

time lag is the main cause of planning and forecasting.

Forecasting is the act of making predictions of future events and

conditions. Forecasting is needed to determine if and when an

event is going to happen so that appropriate planning can be made to control the outcome of this event to a certain extent.

Planning can play an important role in management. Today, almost

every manager who is about to make a decision has to consider

some kind of forecast. Sound predictions of demands and trends

are no longer luxury items, but necessities for managers who need

to cope with seasonality, sudden changes in demand levels, price

cutting operations of the competition, strikes, and large swings

of the economy. Forecasting helps the manager in dealing with

these problems, and it helps best if the manager knows about the

general principles of forecasting, what it can and cannot do

currently, and which techniques are suitable to the needs at any

given time.

To handle the increasing variety and complexity of managerial

forecasting problems, many forecasting techniques have been

must be taken to select the most suitable technique for a

particular application. The manager as well as the forecaster

have roles to play in technique selection and the better

the manager understands the range of forecasting possibilities,

more likely it is that a company's forecasting efforts will

be successful.

The selection of a method depends on many factors. Some of these

factors are the context of the forecast, the relavence and

availibility of historical data, the degree of accuracy

desirable, the time period to be forecast, the cost/benefit (or

value) of the forecast to the company, and the time available for

making these analysis. Forecasting methods are discussed in the

There are two basic categories of forecasting techniques: 1. Qualitative techniques

2. Quantitative techniques

Qualitative techniques can be divided into two types of methods: 1-a. Exploratory methods

1. b. Normative methods

Quantitative techniques can also be divided into two types of methods.

2. a. Time series methods 2.b. Causal methods

1. Qualitative Methods

Qualitative methods use qualitative data such as expert

opinion. These methods are used when data are scare or when no

historical data are available. Qualitative methods can be divided into exploratory and normative methods.

2,2· Forecasting Techniques

l.a. Exploratory methods: start with today's knowledge and its

orientation and trends, and seek to predict what will happen in the future and when. An example is the Delphi Method. It involves circulating a series of questionnaires among individuals who have

the knowledge and ability to participate meaningfully. Responses

Each new questionnaire is developed using any information

extracted from the previous one, thus enlarging the scope of

information on which participants can base their judgements and to achieve a consensus forecast. However, the Delphi Method does

not require that a consensus be reached. Instead, it allows for

justified differences of opinion rather than attempting to

produce unanimity (Brown 1968).

l.b. Normative Methods: these methods begin with the future by

determining future goals and objectives, then work backwards to

see if these can be achieved, given the constraints, resources

and technologies available. An example is the relavence tree

approach. This method uses the ideas of the decision theory to assess the desirability of future goals and to select those areas

of technology whose development is necessary to the achievement

of those goals. The technologies can then be singled out for

further development by the appropriate allocation of resources (Wheelwright and Makridakis, 1980).

2. Quantitative Techniques

Quantitative techniques can be used when the following three

conditions are satisfied:

1. information about the past is available

2. this information can be quantified in the form of numerical

3. it can be assumed that some aspects of the past will continue in the future

Quantitative techniques can be divided into time series methods and causal

methods-2.a. Time Series Methods: a time series is a time-ordered

sequence of observations that have been taken at regular

intervals over a period of time (hourly, daily, weekly, monthly,

quarterly and so on). Analysis of time series data requires the

analyst to identify the underlying behavior of the series. These

behaviors can be described as follows:

♦ trends (gradual, long term movement in the data)

♦ seasonality (short-term, fairly regular, periodic variations) ♦ cycles (wave-like variations of more than one year's duration)

t irregular variations (due to unusual events)

♦ random variations are the residual variations that remain after

all of the other behaviors have been accounted for (William J.

Stevenson, 1986)

There are four approaches to the analysis of time series methods: 1. The naive approach.

2. Moving averages.

3. Exponential smoothing.

4. Decomposition of a time series.

accepted as the forecast for the next period. It works accurately if there is little variation in actual values in time series from period to period.

2. Moving averages: moving average is an average that is

repeatedly updated. As new observations added to the series, the

old observations are deleted from the series. In this way, the

average can be kept current. Moving averages can be simple or weighted moving averages. Simple moving average is the average value of a time series for a certain number of the most recent periods and accepting that average as the forecast for the next

period. Weighted moving average assigns weights to the

observations in a decreasing order from the recent observation to

the oldest one, then takes the average of these weighted

observations as the forecast for the next period.

3. Exponential smoothing: it is a form of weighted moving

average. The name exponential smoothing is derived from the way

weights are assigned to historical data, the most recent values

receive most of the weight and weights decrease exponentially as

the age of the data increases. The method is easy to use and

understand. Each new forecast is based on the previous forecast

plus a percentage of the difference between that forecast and the actual value of the series at that point. That is:

New forecast=01d forecast+ a (actual-old forecast)

This equation is the general form used in computing a forecast

with the method of exponential smoothing. Some of the smoothing

techniques used are as follows: 1. Brown's exponential smoothing

2. Holt's linear exponential smoothing 3. Winter's seasonal smoothing

1. Brown's exponential smoothing: Brown's method uses simple,

linear, or quadratic smoothing to generate forecasts for a time

series. Therefore Brown's method can be examined in three section as follows:

i. Brown's one-parameter adaptive method

ii. Brown's one-parameter linear method

iii. Brown's one-parameter quadratic method

Here, only the first method will be explained briefly·

i. Brown's one-parameter adaptive method: it involves a single

smoothing constant (with a value between 0 and 1), is very

general, and has given satisfactory performance in practical

situations· The equations used in this method are as follows:

Sts=Sti— i+bi"*·(1-r^

bt.=bt:-j. + ( l-r)2 .e^ e,:=Xt.-F.,

r = smoothing constant et=error term

b=trend adjustment

m=number of periods ahead to be forecast t=time

X=actual value F=forecast value

First equation, smooths the current values of the errors. This

approach is a different way of formulating the forecasts, which

can be combined with that of formulating the forecast based on

previous values of the series.

2. Holt's Linear Exponential Smoothing: this smoothing method is

similar in principal to Brown's method except that it does not

apply the straight forward double smoothing formula. Instead, it

smooths the trend values seperately. This provides greater

flexibility, since it allows the trend to be smoothed with a

different parameter than that used on the original series. Holt's

method uses two smoothing constants (with values 0 and 1) unlike

Brown who uses one smoothing constant for forecasting (for more

details see Wheelwright and Makridakis, 1983).

3. Winter's Seasonal Smoothing: It uses three smoothing constants

to generate forecasts for a seasonal time series. This method

involves three smoothing equations one for stationarity, one for

trend, and one for seasonality (for more details see Wheelwrigt and Makridakis, 1983).

The last approach to the analysis of time series methods is

the decomposition of time series.

4. Decomposition of Time Series: in this approach a time series

is viewed as being made up of four possible components: trend,

seasonality, cycles, and random plus irregular variations. This

approach aims to distinguish various components (except random and irregular variations) so their effects can be considered separately. In some situations, interest may focus on only one of these components instead of all of them. For example, a buyer for a department store may be more concerned with seasonal variations in demand than with long-term projections.

The second quantitative technique as mentioned at the beginning of the chapter is the causal methods.

2.b. Causal Methods: these methods assume that the factor to be

forecast shows a cause/effect relationship with a number of other

factors (for example, sales=f(income, prices, advertising,

competition, etc.)). The aim of the method is to discover that

relationship so that the future values of sales can be found using the values of income, price, advertising. Regression models

and multivariate time-series models are the most common

forecasting approaches of causal^ mode l s .

Although the methods discussed above may be suitable for short

term forecasting of time series, we can see cases where the real

life situation is much more complicated, and the pattern is made

up of combinations of a trend, a seasonal factor, and a cyclical

factor as well as the random f lue tuat i ons. In these cases a much

more comprehensive forecasting method is needed. The Box Jenkins

method of forecasting is particularly well suited to

handle this type of real situations (Wheeelwright and

Makridakis, 1980). In addition, forecasts from ARIMA models are

said to be optimal forecasts. This means that no other

univariate forecasts have a smaller mean squared forecast error. This technique is discussed next.

2-3 Box Jenkins Method of Forecasting

George E.P. Box and Gwilym M.Jenkins (Box,Jenkins 1976) are the

two researchers who have effectively put together in a

comprehensive manner the information required to understand and use univariate (single) time series ARIMA models. Univariate Box

Jenkins (UBJ) models are often referred to as ARIMA models. An

ARIMA (Autoregressive Integrated Moving Average) model is an

algebraic statement showing how observations on a variable are

statistically related to past observations on the same variable.

Autoregressive (AR) models are a form of regression, but instead

of dependent variable (the item to be forecast) being related to

independent variables, it is simply related to past values of

itself at varying time lags. Therefore AR models are those that

express the forecast as a function of previous values of that

time series. AR models are first introduced by Yule (1926) and

later generalized by Walker (1931).

MA (moving average) models in Box Jenkins modelling means that

the value of the time series at time t, is influenced by a

current error term and (possibly) weighted error terms in the

past. MA models were first used by Slutzky (1937). Later,

Wold (1938) provided the theoretical foundations of combined

ARMA (Autoregressive Moving Average) processes. In an ARMA

model, the series to be forecast is expressed as a function

of both previous values of the series (autoregressive terms) and previous error values (the moving average terms).

ARIMA models can be used if the following conditions exist in a time series: ARIMA are models suited to short term forecasting because most ARIMA models place heavy emphasis on the recent past

rather than the distant future. ARIMA models are restricted to

data available at discrete, equally spaced time intervals. At

least 50 observations are required as a sample size for this model. Although, the UBJ method only applies to stationary time

series, (i.e. a series that has a constant mean, v a r i a n c B f

and autocorrelation function over time) this is not a

disadvantage. Because, most nonstationary series that arise in

practice, can be converted into stationary series by means

of transformations such as differencing. In ARIMA analysis, the

observations in a single time s e r i e s a r e assumed to be

statistically dependent, that is, sequentially or serially

córrelated.

Box Jenkins approach divides the forecasting problem into three stages:

1. Identification 2. Estimation

3. Diagnostic checking

1. Identification; At the identification stage, estimated

autocorrelation function (acf) and estimated partial

autocorreI ation function (расf ) are plotted. These functions

measure the statistical relationship between observations in a

single data series. The idea in autocorrelation analysis is to

calculate a correlation coefficient. We are finding the

correlation between sets of numbers that are part of the same

series. An estimated autocorrelation coefficient is not

fundamentally different from any other sample correlation

coefficient. It measures the direction and strength of the

statistical relationship between observations on two random

variables. It is a dimensionless number that can take on values

between -1 and +1. Box and Jenkins suggest that the maximum

number of useful autocorrelations is roughly n/4, where n is the

number of observations ( Pankratz, 1983). If the ac f plot

damps out quickly to zeros along the lags, we can say

the series on hand is stationary. If the acf fails to damp out

quickly we suspect nonstationarity.

An estimated pacf is very similar to an estimated acf. An

estimated pacf is also a graphical representation of the

statistical relationship between observations. It is used

as a guide, along with the estimated acf, in choosing one

At the iden t i f ica t ion stage we compare the estimated ac f and рас f

with various theoretical acf's and pact's to find a match. Ые

choose, as a tentative model, the ARIMA process whose

theoretical acf and pact best match the estimated acf and

pact. Once the model has been tentatively identified, we pass to

stage 2, that is, the estimation stage.

2. Estimation: At this stage we fit the model to the data to get

precise estimates of its parameters and we examine these

coefficients for stationarity, statistical significance and

other indicators of adequacy of the model. The t-value measures

the statistical significance of each estimated autocorrelations. A large absolute t-value (|t|>2) indicates that the corresponding estimated autocorrelation coefficient is significantly different

from zero. This stage provides some warning signals about the

adequacy of the selected model.

3. Diagnostic Checking: Diagnostic checking enables the analyst to determine if an estimated model is statistically adequate. The

most important test of the statistical adequacy of an ARIMA

model involves the assumption that the random shocks are

independent. Random shock (at) is a value that is assumed to

have been randomly selected from a normal distribution that has mean zero and a variance that is the same for each and every time period t. In reality it is not possible to observe random shocks,

but we can obtain estimates of them. We have the residuals (estimated random shocks) calculated from the estimated model.

The basic analytical tool in diagnostic checking stage is the

residual a c f . It is the same as any other estimated acf· The only difference is that we use the residuals from an estimated model instead of the observations in the time series data to calculate the autocorrelation coefficients. The idea behind the use of the

residual acf is that, if the estimated model is properly

formulated, then the random shocks should be uncorrelated. When

the residuals are correlated we must consider how the estimated

model could be reformu1 ated. Sometimes, this leads us back

to the identification stage. We repeat these steps until we find a good model.

2.4. Common ARIMA Processes

An ARIMA process refers to the set of possible observations on a

time sequenced variable, along with an algebraic statement (a

generating mechanism) describing how these observations are

related. The generating mechanism for five common ARIMA

processes are written as follows:

AR(i) MA(1) AR(2) MA(2) 2 tr = C+( #JL ) . z z^=C-(ej.) ) . z ia ) . Zt-2-*-at z ( 0 i ) .at — i“ (02) .at—

izt = AR coefficients

Oi, O2 = MA coefficients

at = random shock at time t C = constant

Zt = numerical value of an observation at time t

C H A P T E R 3 A P P L I C A T I O N OF BOX J E N K I N S M E T H O D U S I N G A M E R I C A N D OL LA R P R I C E S

In this chapter, the daily asked prices of American

Dollar in terms of Turkish Lira is analyzed by Box-Jenkins

method. For this purpose, a package called Statistical Graphics

System (Statgraphics, version 2.1) is used. There are 794 daily

observations covering the period, September 1985 till

December 1988. The data is based on 5 working days

per week excluding Saturdays and Sundays. Major part

of the data is obtained from Turkey's Central Bank.

The time sequence plot of this observations is shown

in Figure 3.1. The vertical axis (diadollar) shows the daily

Dollar prices and the horizantal axis is a time scale of

workdays.

In Box Jenkins analysis, it is supposed that the time sequenced

observations in a data series may be statistically dependent.

Therefore, the statistical concept of correlation is used to

measure the relationships between observations within the series.

That is, the correlation between z (numerical value of an

observation) at t (time), and z at earlier time periods is

examined. This analysis is started with an assumption that Dollar

prices for any given time period may be statistically related to

prices in earlier periods.

It is understood from visual analysis of the time sequence plot of dollar (Figure 3.1.) that, its mean is not stationary, because

the series trends upward overtime. The single mean for this

series is calculated. It is 907.526 (Table 3.2.). However, this

single number is misleading because, major subsets of the series

appear to have means different from other major subsets. For

example, the first half of the data set lies below the second

half. The variance of the series seems to be roughly constant

overtime.

3 . 1 . Iden ti fication

The estimated autocorrelation function (acf) is plotted for

this series (Figure 3.2). Pankratz (1983) suggests that the

maximum number of useful estimated autocorrelations is

roughly equal to the number of observations divided by

four. With 794 observations 198 (794/4) autocor

relations can be calculated and shown in Figure 3.2. The

vertical axis shows autocorrelations and horizantal axis shows

lag. Lag is the number of time periods separating the ordered

pairs used to calculate each estimated autocorrelation

coefficient. The estimated acf for this observation decays to

zero very slowly indicating a nonstationary mean. Differencing is

used when the mean of a series is changing overtime, and

therefore the original dollar series (Figure 3.1) is differenced

once, as shown in Figure 3.3. This way, the differenced dollar series has no longer a noticeable trend.

A series which has been made stationary by differencing

has a mean which is virtually zero value. The differenced

series in Figure 3.3 has also a mean of zero as can be

seen in Table 3.3. Now then, the series is stationary, with

a mean of zero and roughly constant variance overtime.

The estimated acf and partial autocorrelation function (pact) for

the first differenced series are plotted (Figure 3.4. and Figure

3.5.). The maximum number of useful autocorrelations are 189

(757/4). Because the original series is differenced, there

are 757 observations that are available (Table 3.3). In reality,

one observation is lost in each differencing, but in the dollar

data there are some missing values and they are causing the

data to loose more than one observation.

The length of each spike is proportional to the value of

corresponding estimated autocorrelation coefficient. The

horizontal lines are placed about 2 standard errors above and

below zero and show how large each estimated autocorrelation would have to be to have an absolute t-value of approximately 2.

Any estimated autocorrelation whose spike extend past the

horizontal line has an absolute t-value larger than 2.

Larger t-value indicates that the corresponding

estimated autocorre 1 ation is significan11y different

from zero, suggesting that true autucorrelation is non

zero. The acf for the first differences moves toward zero more

quickly than the acf for actual data (Figure 3.2.). But the

decline is still not rapid. The first, second, fifth and tenth

autocorrelations are significantly different from zero. There are some others passing the horizantal line but they are very small

relative to the ones mentioned above, therefore they can be

omitted from analysis.

The pattern of the acf plot is similar to the theoretical acf of

an autoregressive model (AR). Because the acf pattern decays to

zero. A decaying acf is also consistent with a mixed

autoregressive moving average model (ARMA). But starting with a

mixed, model is not practical and unwise in Box Jenkins model,

because of principle of parsimony, which uses the smallest

number of coefficients needed to explain the available data.

Identify the order of the AR model, the estimated pacf plot

(Figure 3.5.) is examined. The estimated pacf is unambigious when

it is compared with theoretical pacfs, and it has significant

spikes at various lags. The pacf spike at lag 5 can be ignored

for the time being, because an AR model of order 5 is unusual.

The pacf plot has two spikes initially then a cut off to zero

like as in the case of theoretical pacf of AR(2). Therefore,

I tentatively select an AR(2) model to represent the data. Now, it is possible to pass to the estimation stage.

3.2. Estimation

In this stage, Statgraphics program estimates the AR coefficients

estimates, standard errors, t-values for the tentative model

(Table 3.4). By the help of these data stationarity of the

first differenced series can be checked numerically. For an A R (2)

model to become stationary following conditions should be

satisfied. AR(2) coefficient should be less than one. The

summation of coefficients (A R (1)+AR(2)) should be less than one.

The difference between these coefficients should be less than

one. According to the Table 3.4. AR(2) coefficient is equal to

0.11145. The summation of AR(1) and AR(2) coefficients is equal

to 0.2252 (0.11145+0.11375) and the difference between these

coefficients is equal to —0.0023 (0.11145—0.11375). In addition, i

AR(1) and AR(2) coefficients are also significantly different

from zero, since their t-values are greater than 2

(2.95346;3.06070). As a result, this model satisfies the

stationarity requirements and it is possible to go one stage further, diagnostic checking stage.

3.3. Diagnostic Checking

In this stage, we decide whether the estimated model is

statistically adequate or not. A statistically adequate

model is one whose random shocks are statistically independent,

meaning not autocorrelated. In practice, random shocks can

be estimated, but not observed. We have the residual random shocks calculated from the estimated model. These residuals are

used to test hypothesis about the interdependence of the random

shocks. If the residuals are statistically dependent, another

model must be found whose residuals are consistent with the

interdependence assumption.

As it is understand from the above paragraph, the basic tool at

the diagnostic checking stage is the residual acf. The estimated

residual acf is shown in Figure 3.5. If the random shocks are

uncorrelated, then their estimates should also be uncorrelated on the average.

According to Figure 3.6, estimated residual autocorrelations

in 3th, 8th, 21st, 175th, and 180th spikes exceeding the

horizontal line above and below zero, falling more than ^2

standard deviations away from the mean of residuals. Sometimes

this happens when data is recorded incorrectly. Since the data

covers the black market prices of dollar, there might be mistakes

in it, although most of the data is taken from the

Central Bank. Besides this, black market prices of currencies are

changing from one newspaper to another. Therefore it is very

difficult to obtain a completely correct data set.

Government intervention policies to black market in Turkey can

cause a large deviation among the observations. For example, in

October 18, 1988 government intervened the black market and

caused a decrease in dollar price from 1985.OOfL/'^ to

1690.00TL/$ (Figure 3.1). Dollar price reached again

1985.00TL/S in March, 0,1989. Time sequence plot of residuals is

shown in Figure 3.7. As it is seen from this plot residuals

appears with large deviations from the mean after the year 1907.

Residuals are followed a stable path from its beginning (1985)

till 1987. In addition, the residuals are calculated from a

sample (one subset of observations) using only estimates of the

ARIMA coefficients not their true values. Therefore, we expect

that sampling error wil cause some residual autocorrelations to

be nonzero even if we found a good model. Sometimes, large

residuals can occur just by chance (Pankratz, 1983). All

of .the above could be the reasons of significant spikes in

estimated residual acf.

Other types of models are also used to obtain better residual

autocorrelations. For example, using the ARMA(1,1) model, it is

observed that the t-value is low for this mixed model relative to AR(2) model. Finally, we decided that AR(2) is more suitable than

the other models and so forecasts will be obtained using this

model.

3.4. Forecasting

The objective of Box Jenkins approach is to find a good model and

to obtain future forecasts of a time series based on this model·

It is assumed that an ARIMA model is known, that is

the mean, AR coefficients and all past random

shocks are known. In reality, this assumption is valid if the

identified and estimated model is adequate. Therefore, the true

mean is replaced by its estimated mean, past random schock values

are replaced by their corresponding estimates. Similarly,

AR coefficients are replaced by its estimates and past

observations are employed for making forecasts.

ARIMA models include integration procedure and it corresponds to

the number of times the original series has been differenced.

Since the dolar series has been differenced once, it must

subsequently be integrated one time to return to its original

form. Observations start from September, 1985 and are

available up to December, 1,1988. The forecasts begins from this

data till to the end of February, 1989. The forecast values are

shown in Table 3.5. By this procedure, we calculate 64 point

forecasts (single numerical forecast values) and their upper and lower values.

Since an appropriate ARIMA model is estimated with a sufficiently

large sample, forecasts from that model are approximately

normally distributed. We can therefore construct confidence

intervals around each point forecast and can plot a forecast

function with 95 percent limits. The plot of forecast function

appears in Figure 3.0. In addition, actual dollar prices is

plotted in Figure 3.9. which corresponds to the forecast period.

Both plots are showing an upward trend. In Chapter 5, we also

calculate the mean absolute deviation (MAD) between forecasted

and actual observations since the visual inspection of these

plots are not sufficient.

Finally, we decide to hold all the data available for the

period September, 1985 till the end of February 1989

in order to forecast the future values of American

Dollar. We again follow the same procedure in the first

case. There are 858 daily observations (dollar prices in

terms of T L ) available (Table 3.6). Time sequence plot

is · shown in Figure 3.10. As it is seen from the

figure the trend of the observations continue upward (last

portion of Figure 3.10). Although the single mean value

calculated is 957.82 (as seen in Table3.6) the mean is not

stationary again. There is no need to take acf plot of the data

set, because it is plotted for the previous case in Figure 3.2.

In the identification stage, the data set is differenced once.

First difference time sequence of plot of observations appear in

Figure 3.11. The mean value is dropped to zero (Table 3.7.).

Therefore, it can be said that the data set is stationary with a

mean of zero and roughly constant variance. The estimated acf and pacf is plotted for the first d i f f e r e n ce series (Figure 3.12 and

3.13) for 205 (821/4) useful estimated autocorrelations. Number

of observ a t i o ns are dropped from 858 to 821 (Table 3.7) due to

first d i f f e r e n c i n g and missing values. As it appears in Figure

3.12. there are m any significant autocorrelations passing the

hor izontal line, compared to the first case (Figure 3.4). The

acf p a t t e r n decays to zero very slowly and therefore, it is assumed tentatively an AR model. The pacf plot (Figure 3.13) very similar to pacf plot in Figure 3.5. So, the order of the model is selected as 2 as in the first case.

Est i m a t i o n results are shown in T a b l e 3.8. AR(2) coefficient is equal to 0.09694. The summation of AR(1) and AR(2) is equal to 0.2 1 49 9 (0.09694+0.11805). The d i f f e r e n c e between AR(2) and AR(1)

is equal to -0.0211. So, this model satisfies the stationarity

c o nd it i on s and ready for d i a gnostic checking.

For d i a g n o s t i c checking the e stimated residual acf is plotted

(Figure 3.14). There are some spikes (2nd, 7th, 19th, 25th and

27th, etc...) which are exceeding the horizantal line above and

b e l o w zero. The same discussion as in the first case is valid

here also. But in this case the point forecast values

inclu d in g the first forecast val u e ( shown in Figure 3.9)

are all c o m pletely out of range. In addition, the

plot of forecast function (Figure 3.15) appears as a straight

line and the last part of the curve is located on the horizantal

axis. The shape of the forecast curve explains why point forecast values are all out of range. The residuals are plotted in Figure

3.16 and it is seen that the added observations (December 1988,

J a n u a r y and February 1989) shows too much variation away from the /

mean. At this point, I tried other models /to obtain good

forecasts as follows:

First, the observations are differenced twice with the same AR(2)

model. Although this model gives an AR(1) coefficient w hi c h has

str on g l y correlated t-value of -18.48785, the forecast va lue s are c o m p le t el y out of range and the forecast function plot is shown in Figure 3.17. It is worst than the first differe nced AR(2) modisl. Therefore, this model is rejected. Then, a mixed model is

tried. It is AR(2)+MA(1) model for the first d ifferenced series.

In this case, the AR(1), AR(2) and MA(1) coefficients have

t-value s less than 2. This model is rejected too. As a result, it

is not possible to find a good model for the updated doll ar price series with Box Jenkins model.

CHAF^TER 4 APPLICAflON OF BOX JENKINS METHOD USING GERMAN MARK

This chapter is focused on the analysis of daily prices of German

Mark in terms of Turkish Lira by Box Jenkins method. The data

covers the period September 1985, till December 1908. A total of

796 observations are available (Table4.1). The time sequence

plot of observations are plotted is shown in Figure 4.1. As it is

seen from the Figure the level of observations are rises through

time. This indicates that the series may not have a stationary

mean. The overall mean for this series is 462.479 as given in

Table 4.1. However, autocorrelation analysis is required

in order to be sure whether this series is stationary or

not in identification stage.

4.1. Identification

Estimated autocorrelations are plotted in Figure 4.2 with 199

(796/4) maximum useful number of autocorrelations and it is

observed that the series has a nonstationary mean. (Since

autocorrelations decays to zero very slowly). Therefore we should

calculate the first differences, then look at the estimated acf.

Figure 4.3 shows the first difference plot of the mark series

for 190 (761/4, Table 4.2) autocorrelations. The estimated acf

moves toward zero more quickly relative to the acf of original

series (Figure 4.2). But it has some significant spikes which

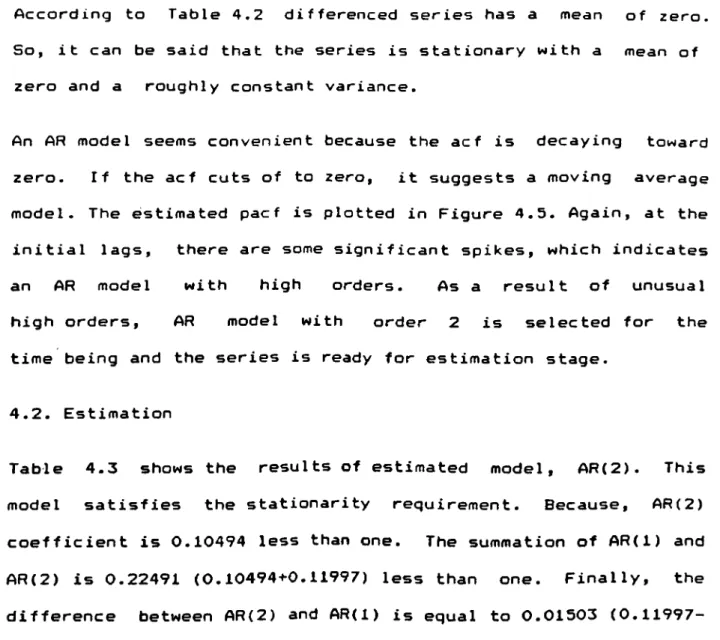

30, then it has all insignif ican t spikes decaying to zero. According to Table 4.2 differenced series has a mean of zero. So, it can be said that the series is stationary with a mean of

zero and a roughly constant variance.

An AR model seems convenient because the acf is decaying toward

zero- If the act cuts of to zero, it suggests a moving average

model. The estimated pacf is plotted in Figure 4.5. Again, at the

initial lags, there are some significant spikes, which indicates

an AR model with high orders. As a result of unusual

high orders, AR model with order 2 is selected for the

time being and the series is ready for estimation stage.

4.2. Estimation

Table 4.3 shows the results of estimated model, AR(2). This

model satisfies the stationarity requirement. Because, AR(2)

coefficient is 0.10494 less than one. The summation of AR(1) and

AR(2) is 0.22491 (0.10494+0.11997) less than one. Finally, the

difference between AR(2) and AR(1) is equal to 0.01503 (0.11997*- 0.10494) less than one. So, the first differenced mark series can

be exposed to some diagnostic checking.

4 . 3 . Diagnostic Checking

Residual acf is plotted and shown in Figure 4.6. These residuals

are estimates of the unobservable random shocks in model AR(2).

As it is seen from Figure 4.6, some residual autocorreIations are

significant. At this point, the Mark series is returned to the

identification stage for trying another ARIMA models for

obtaining uncorrelated residuals. But at the end, it is realized

that some significant autocorrelations remain in residuals

whatever the estimated model. Then, it is decided that,

significant residual autocorrelations are occur due to some

sampling error, misrecorded data, and government intervention

policies to black market etc... In addition, time sequence plot

of residuals (Figure 4.7) shows a strong variation after the

year 1987, like in the case of analysis of residuals of American

Dollar (Figure 3.7). So, the forecast values will obtained by

using AR(2) model in forecasting stage.

4.4'Forecasting

Forecasts for AR(2) model, for the period December 1988, January

and February 1989 (64 point forecasts) are shown in Table 4.4 with two additional columns besides forecasts. They are for lower

and upper limits of forecast values. The forecast values is

plotted in Figure 4.8 with 95X limits, it shows an upward

trend. The actual observations are drawn in Figure 4.9. It is

very different than the forecasted plot because, government

intervention exists in this period. In addition, MAD value

(calculated in Chapter 5) comes out to be a large value which

indicates less accuracy of this forecast model.