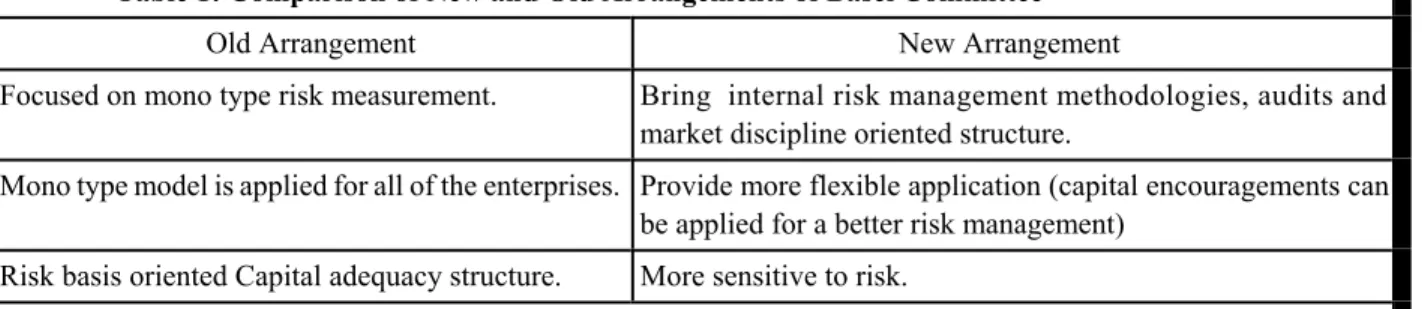

Globalization of financial markets and reflexion to Turkish small and medium scale enterprises: Basel II

Tam metin

Şekil

Benzer Belgeler

The reward-to-risk ratios presented are Sharpe ratio (Sharpe), non-parametric value at risk based Sharpe ratio (VarSharpe) and parametric value at risk based Sharpe ratio

This study investigates the significance of return on assets, return on equity, capital adequacy ratio, operating efficiency ratio, gearing ratio, networking capital, loan

Is there a statistically significant relationship between bank‟s size and capital adequacy ratio in Islamic banks.. The second main question which focus on

In the first step, we test separately the impact of operational risk proxied by the capital charges within the Basic Indicator Approach (KBIA), loans activity (credit risk)

Şut atışı (sabit ayağı toplam 20-30 cm uzaklıkta yanına koymak) İlave görev (dominant ayağın dokunma alanı: ayak içi). Direktif (sabit ayağını topun uzağına yanına koy

Tanınmış Türlr ressamı Fah büyük sar.-'t kabiliyetiyle cosı Prens Zeyd Berlin’de elçi olarak bulunduğu sıralarda jita gibi tanınmış ressamların Alman

Yalı köyünün, meş hur çayırın kenarından geçilip sağa sapılır; bir müddet gittik ten sonra yine sağa çarh edilip iki tarafı çınarlarla sıralanmış

[r]