Comparison of loan default : participation versus conventional banks in Turkey

Tam metin

Şekil

Benzer Belgeler

Düzce Üniversitesi Araştırma ve Uygulama Hastanesi Kardiyoloji ve Acil polikliniklerine, 2006-2008 yılları arasında göğüs ağrısı şikayeti ile ardışık

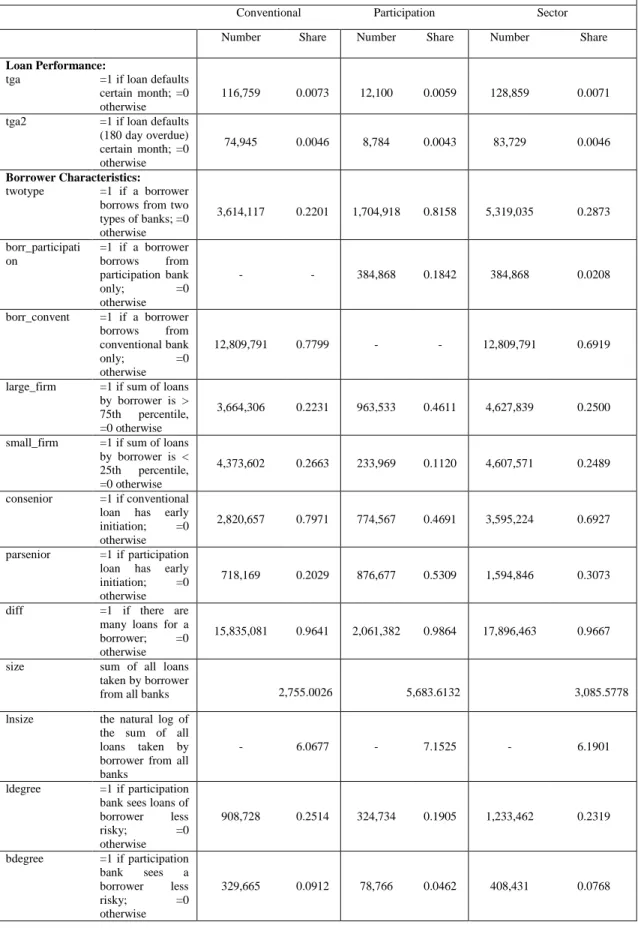

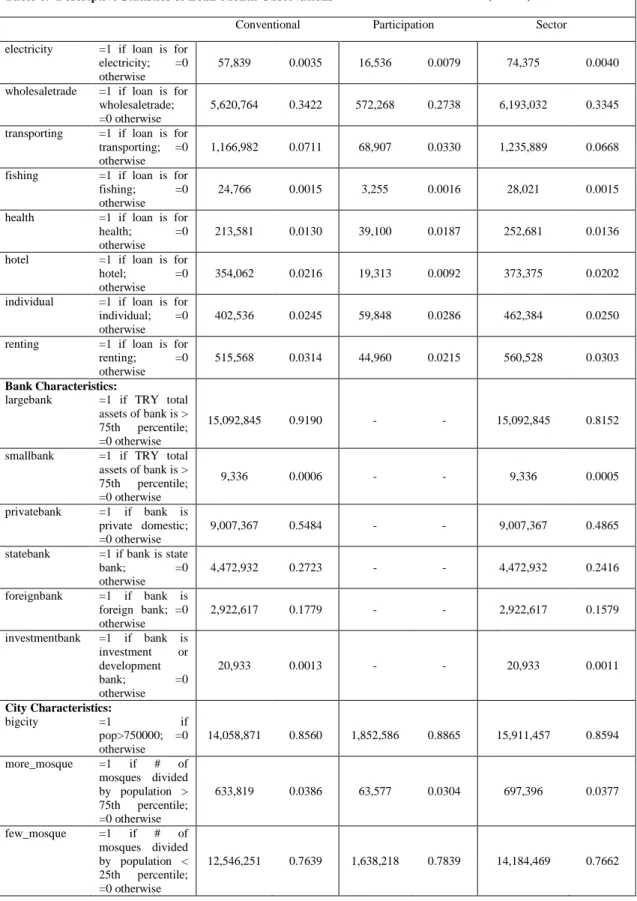

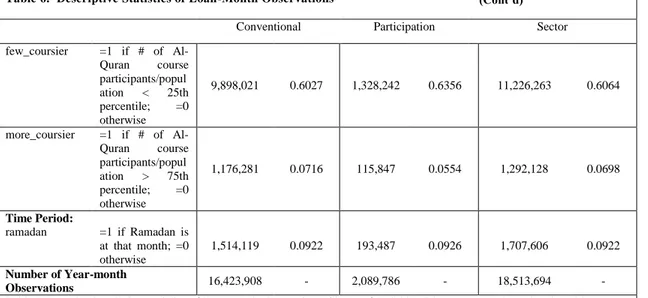

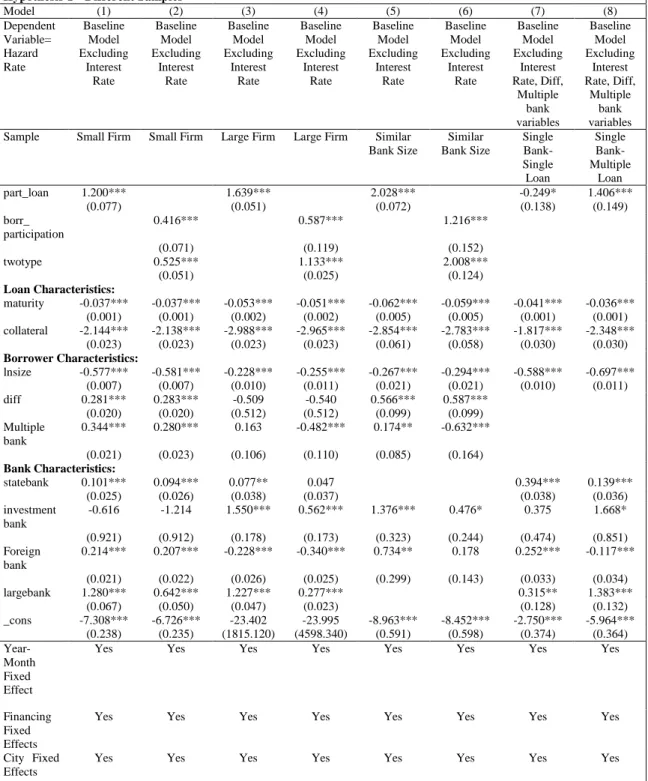

The panel data collected from Bank scope for the banks included in our study is used to make a regression analysis in order to investigate the determinants of credit,

Applying E-views software some correlation and regression analysis were carried out on data and tried to find out the impact of some independent variables

In the analysis of the profitability ratio (ROA & ROE) of Islamic and conventional banks made by Ansari and Rahman (2011) in Pakistan during 2006-2009, their study showed

[r]

Güney Kore 1960’lı yıllardan itibaren oluşturduğu iktisat politikaları ve bunu tamamlayıcı teknoloji politikaları uygulamaları ile birlikte, 1990’lı yıllara

Aşağıdaki noktalı kağıda farklı boyutlarda ikişer adet paralelkenar, eşkenar dörtgen ve yamuk

Therefore, these observations imply that the lending behavior of Islamic banks are immune to and lending growth of conventional banks is negatively affected by economic