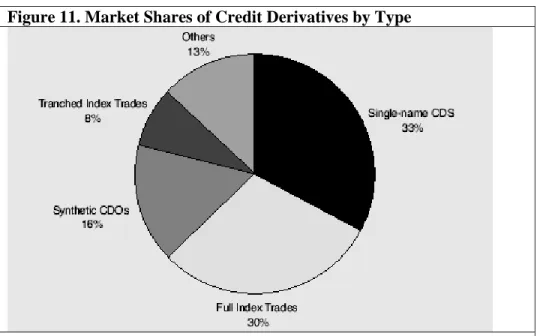

Credit default swap (CDS) ındexes and their usage in risk management by Turkish banks

Tam metin

Şekil

Benzer Belgeler

• C tipi uçucu kül ile üretilen ve ortam sıcaklığında kürlenen geopolimer betonunun mekanik özelikleri benzer dayanıma sahip çimento esaslı betona göre yakın

[r]

Koska, Ayasofya (yani Alemdar), Voyvoda, Okçumusa yokuşlarına gelin ce mecvud bir çift veya iki çift beygirin öniine iki tane daha eklenir; seyis avu cuna

The aim of the study was to analyse AMH concentrations under the guidance of circulating estradiol and progesterone levels in mares.. The study was conducted on 25 non-lactating

Ancak Ortadoğu, Sudan, Kenya ve Somali’den elde edilen deve izolatları ile yapılan moleküler çalışmalar ile, deve izolatlarının koyun ve sığır izolatları ile

Benzer şekilde soya fasulyesi tohumlarına yapılan melatonin uygulamalarının fidelerin tuz stresine karşı toleranslarını arttırdığı ortaya konmuştur (Wei ve ark.,

Tarihi özelliklere sahip kentsel bir doku içerisinde kente yabancı bireylerle gerçekleştirilen bu çalışmada bulgular; taslak haritaların ağırlıklı olarak ardışık tarzda

Ankara’nın Kıışcağız Gecekondu Mahallesinde Gocukların