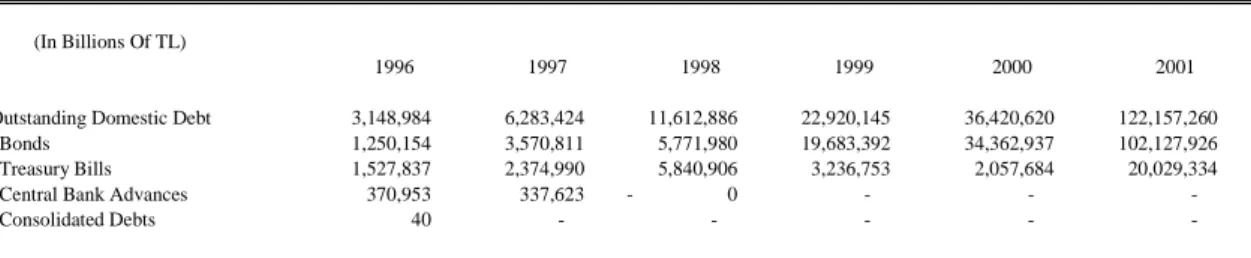

Central Bank balance sheet and predictability of financial crises 2001 Turkish case

Tam metin

Şekil

Benzer Belgeler

Autocratising countries underperformed for all three outcome variables in the 10 years after the onset of autocratisation, despite some improvements in life expectancy, UHC

treated SpDSp-PA nanofibers, since enhanced osteogenic dif- ferentiation was observed on these peptide nanofiber surfaces. In addition, we observed that different medium conditions may

We show that in a ‘‘p53 network’’ application, the proposed method effectively detects anomalous activated/inactivated pathways related with MDM2, ATM/ATR and RB1 genes, which

Furthermore, the number of attached cells was doubled on the non-coated patterned CNT sur- faces when compared to collagen coated patterned surfaces, where collagen coating acted as

Finally, the last example compares the performance levels of finite dimensional controllers by using an approximation of an infinite dimensional plant and the new structure, which

Çalışmanın son bölümünde, gözönüne alınan parametrelere ait alt ve üst sınırlar dahilinde seçilen betonarme köprü kolonlarının moment – eğrilik analizlerinden

The status of Syrian Kurds, the political future of Bashar al Assad, the presence of Turkish forces in Northern Syria, divergent positions over Idlib and Russia’s ties with Iran

The width of the fabricated patterns is not only defined by the diameter of NFs, but also by the extent of spreading during the thermal annealing step, which is necessary for