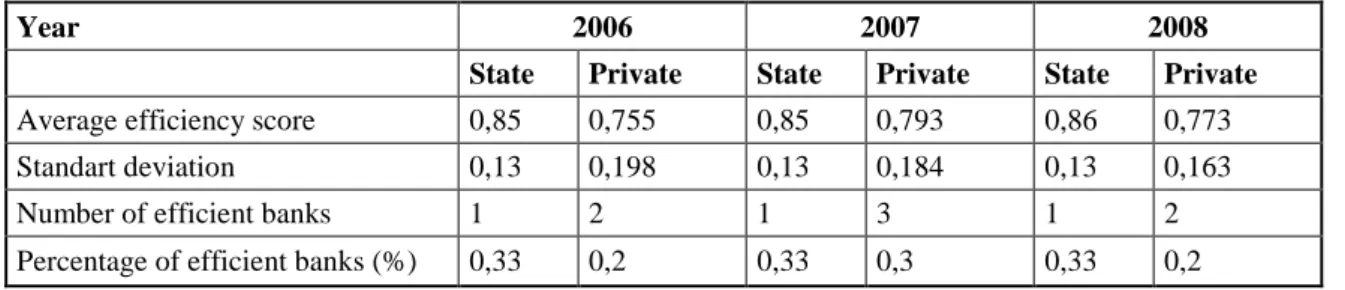

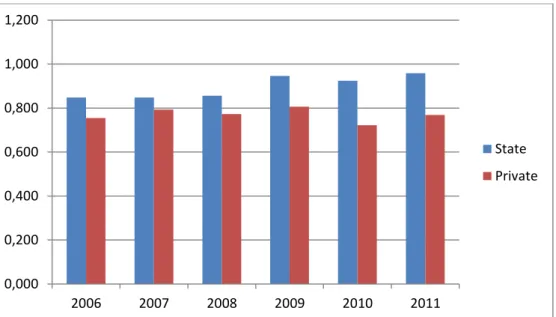

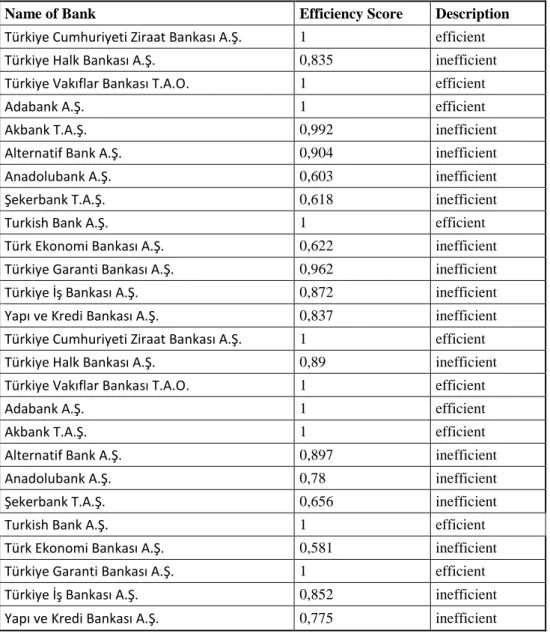

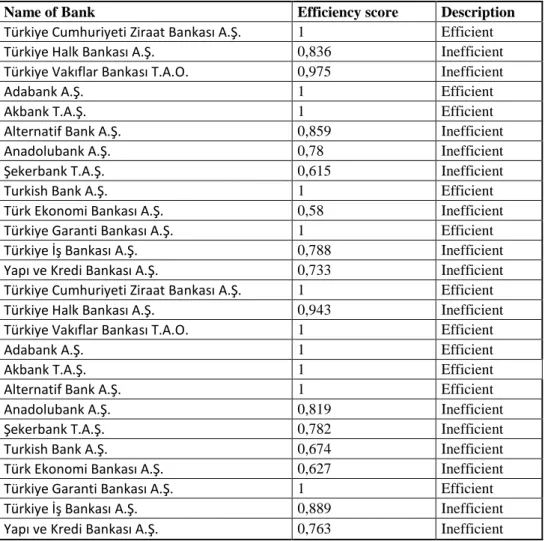

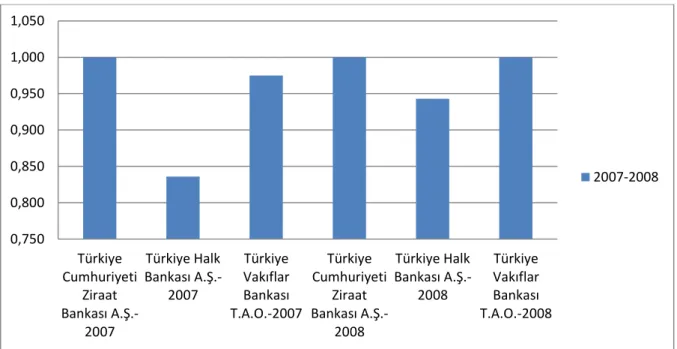

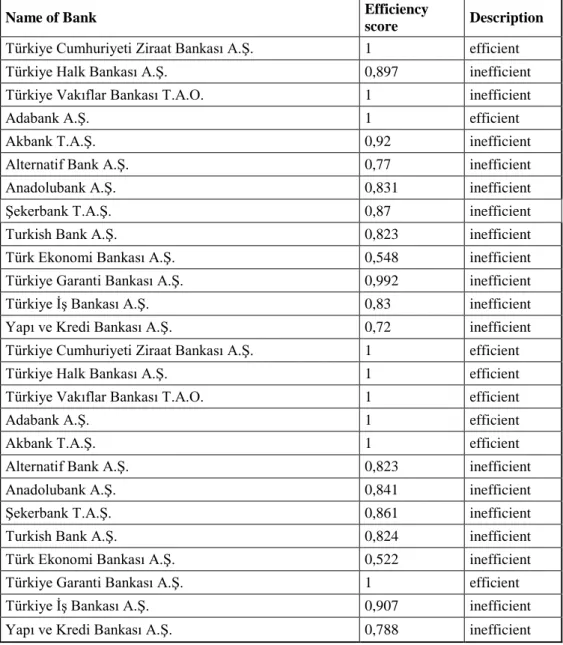

Efficiency in Turkish banking industry: A comparison of state-owned and privately-owned banks

Tam metin

Şekil

Benzer Belgeler

Kurum kimliğini varılması gereken hedef, olarak nitelendirdiğimizde bu hedefe yönelik çıkılacak yolculukta kurum kültürü çıkış noktası, kurum imajı alınan yol, kurum

Compared to controls, PTSD group had bilaterally smaller hippocampus, amygdala, anterior cingulate cortex, and thinner prefrontal cortex with no difference on thalamus ( Table 2

From that perspective, in the second part of this study, starting from the half of the second chapter I will try to have a close look at Eve Kosofsky Sedgwick’s essay “Paranoid

Genel olarak daha çok Aydın İli Nazilli İlçesi sınırları ve küçük bir kısmının da İzmir İli Beydağ İlçesi sınırları içinde yer alan Oyukbaba dağı ve

Further experiments indicate that resulting OCR errors have limited effect on informa- tion retrieval (IR) performance; therefore the proposed framework can be used as a building

Karaman ve ark.'nın geriartik hastalarda yapılan ortopedik cerrahi uygulanan hastalarda yaptıkları bir çalışmada rejyonel anestezi alan grupta yoğun bakımda

Bilgisayarlı tomografi teknolojisindeki son gelişmeler göz önüne alındığında kalp nakli yapılan hastalarda allogreft vas- külopatiyi değerlendirirken öncelikle BT

Devlet memurluğuna alınamazlar.”.. maddesi hükümleri, seçimler dışındaki bir sebeple ayrılanların dönmesine ilişkindir. Seçimlere katılmak üzere istifa edenlerin