Determinants of Currency Crises in Turkey

Tam metin

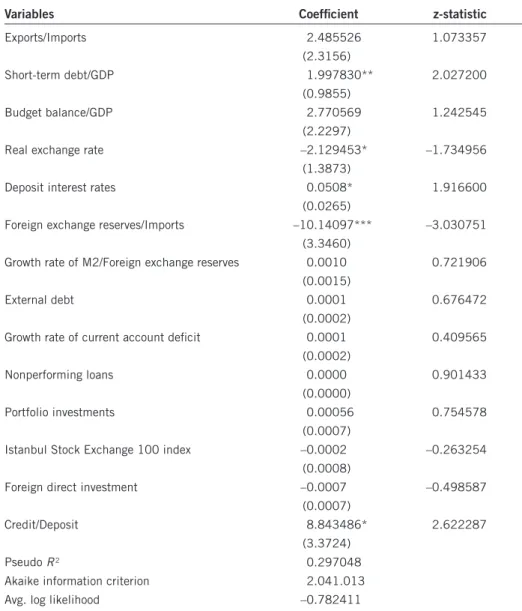

Şekil

Benzer Belgeler

İki ya da daha fazla kelimenin gerçek anlamlarından uzaklaşarak başka bir anlam taşıyacak şekilde kalıplaşmasına deyim denir.. Aşağıdaki deyimleri

Diye elçi gönderdi; Sultan Meh med de ol sığır derisinden kestiği sırımı Kostantine gönderip:.. — İşte biz şikârhanemizi bir sığır derisi cirminde

The system uses naive Bayes classifiers to learn models for region segmentation and classification from auto- matic fusion of features, fuzzy modeling of region spatial re-

The simulation of the scene (determining particle neighborhood information, computing fluid pressure-based forces, computing two-way coupling forces, and interpolat- ing

• Güngöroğlu (2018)’e göre; Yenice Ormanları orman ağaç türleri bakımından çok zengin ve burada bulunan Kavaklı Tabiatı Koruma Alanı’nda toplam 176 bitki taksonu

Lokal komplikasyon gelişen olgular haricinde profilaktik antibiyotik verilmesi tartışmalı olsa da yılan ağız florasında çok çeşitli aerob-anaerob

The Ternan girls were defined as “quick eyed,” “industrious,” “sharp,” “aspiring,” and “clever,” (Tomalin, 1991, p. 165) when women in the Victorian period..

Given this particular historical background of autobiography and memoir publishing in Turkey, and the connections drawn by contemporary conserva- tive historiography with