The Re-making of the Turkish Crisis

Tam metin

Şekil

Benzer Belgeler

Nazmi Ziya’nın “ Sultan Tepeden Bakış” adlı yağlıboya çalışması 22 milyar 500 milyon T L ile müzayedenin en yüksek açılış fiyatına sahip. Müzayede

Poliakoff, Archipenko, Hartung ve Zadkine gibi Paris Ekolü'nün önde gelen sanatçıla rıyla birlikte sergiler açan Anlı'nın eserlerinin bulunduğu müzeler şunlar:

Gerçek yaşam verisi/Real world data...1*suppl (73) Görüntüleme/Imaging ...1*suppl (54) Hidroksiklorokin/Hydroxychloroquine ...88 HLA-B*27/HLA-B*27 ...1*suppl

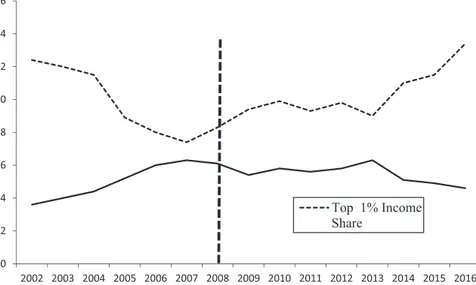

In other analyzes of the Revolution in Iran, the researchers, trying to put forward the relationship between economic problems and the Revolution, are trying to

Diffuse idiopathic pulmonary neuroendocrine cell hyperplasia (DIPNECH) is a rare disease which needs a long time for diagnosis and usually defined by case reports and small series..

The nanoparticles were prepared either via Cu-catalyzed or cucurbit[6]uril (CB6)-catalyzed click reactions between azide groups containing hydrophobic blue, green and yellow

The width of the fabricated patterns is not only defined by the diameter of NFs, but also by the extent of spreading during the thermal annealing step, which is necessary for

Fren test cihazının rulman arızaları, titreşim analiz yöntemi Vibrotest 80 model titreşim ölçüm cihazı ile düzenli olarak aylık periyotlarda, fren test cihazı