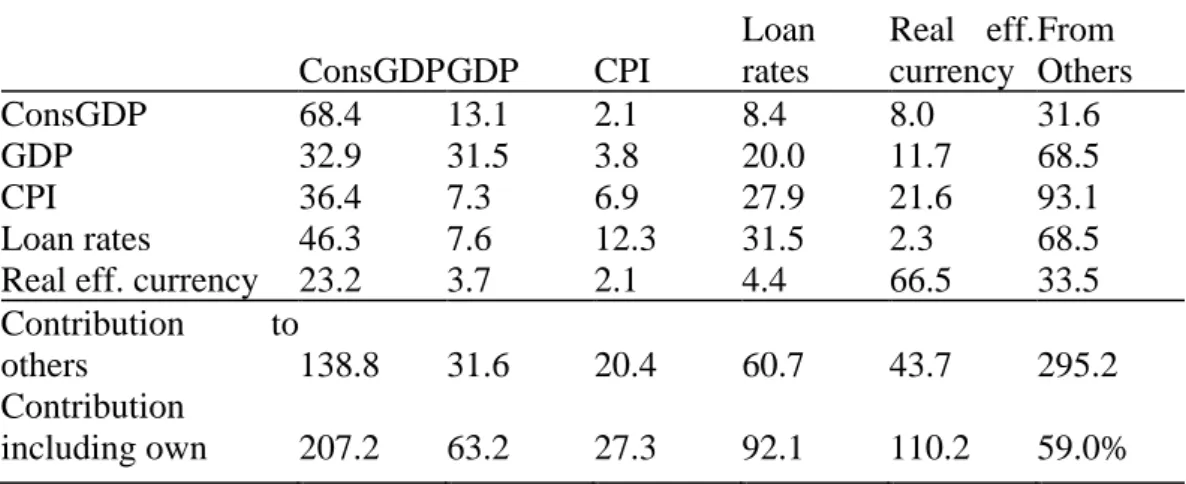

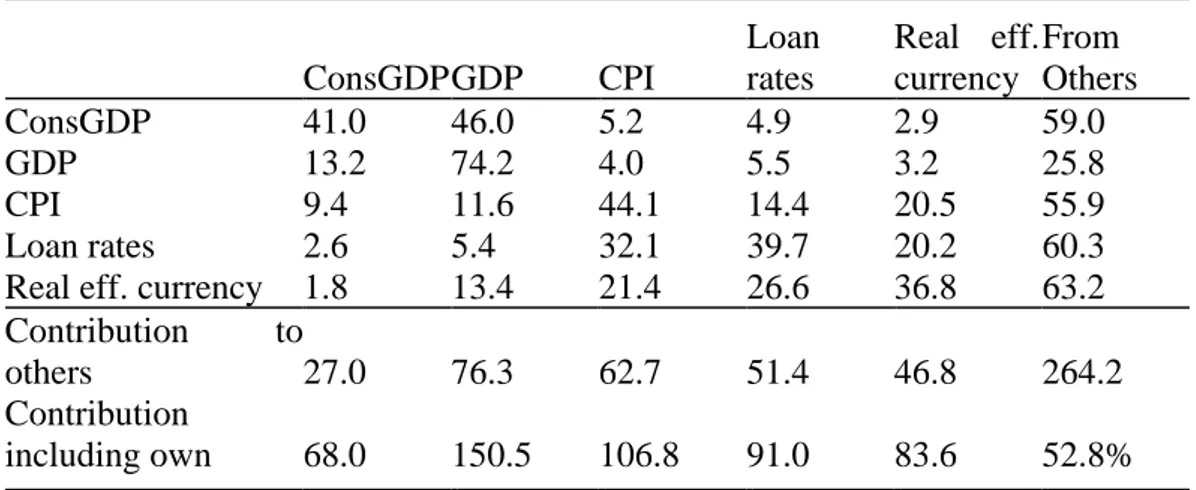

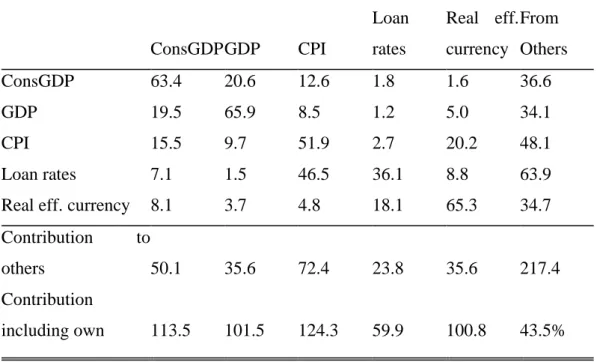

Construction GDP and total GDP in Turkey: before&after the global crisis analysis

Tam metin

Şekil

Benzer Belgeler

Kitapta anlatılan Çetin Altan - Melih Cevdet Anday kavgasının tanığı olan gazeteci- yazar Mine Kırıkkanat, Hıfzı Topuz’un bazı olayları yanlış

Benzer süsleme tekn;~inde yap~lm~~~ ve Kusura örne~i gibi sa~lam ele ge- çen bir ba~ka testi ise (~ek. Bugün Afyon Müzesi'nde korunan E.7439 envanter numaral~~ bu testi, biçim

1672 tarihine kadar eski harb usulü oian (rampa) devam etmekle beraber rampa dan evvel toplarla düşmana mümkün ol duğu kadar telefat verdirmek, şaşırtmak da

According to the second research strand which draws the long-run relationship coefficients where energy consumption is dependent while CO2 emissions and GDP per capita

Aga (2014) researched on The Impact of Foreign Direct Investment on Economic Growth in Turkey he analyse the impact by using time series techniques, by choosing The gross

Ultimately, the Granger test revealed that there is no evidence in this study for the finance led growth hypothesis; there is a unidirectional causality running from trade to

Increases in price will negatively affect oil demand in a long-run especially for oil importers such as the OECD and Real GDP positively affects demand for

For the first part of the paper, the calculation of the GDP loss due to low female labor force participation is as the following. For all three parts the