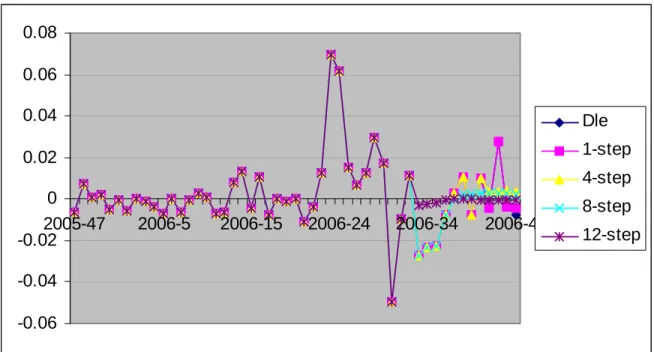

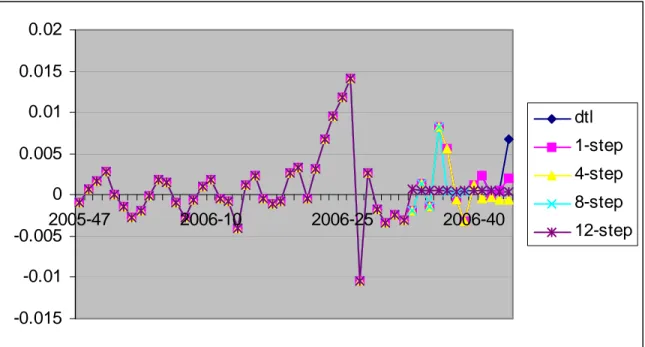

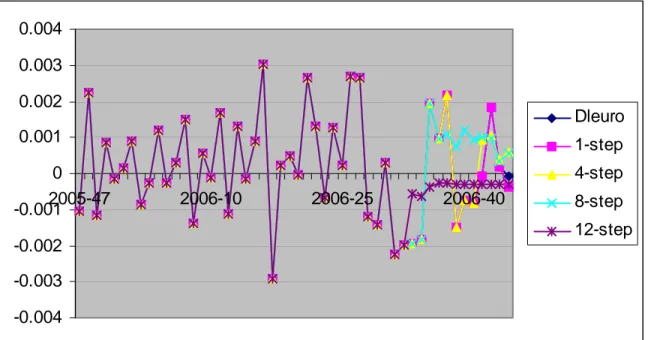

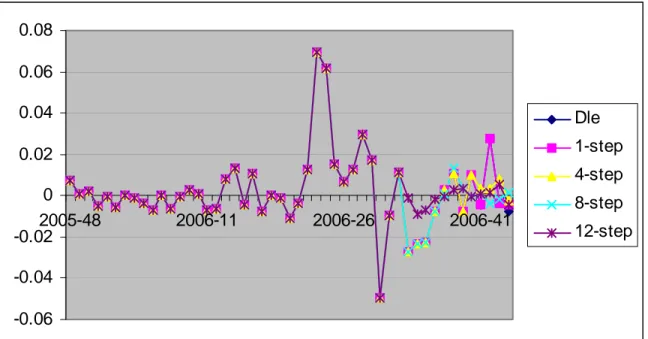

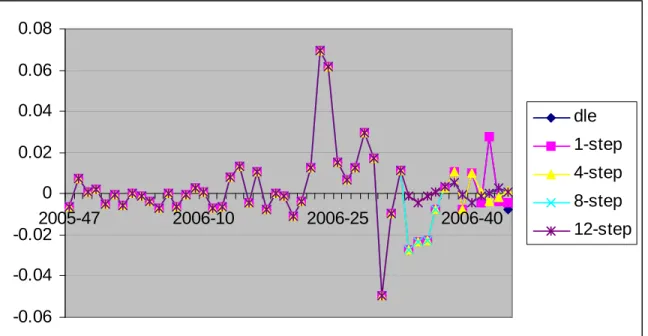

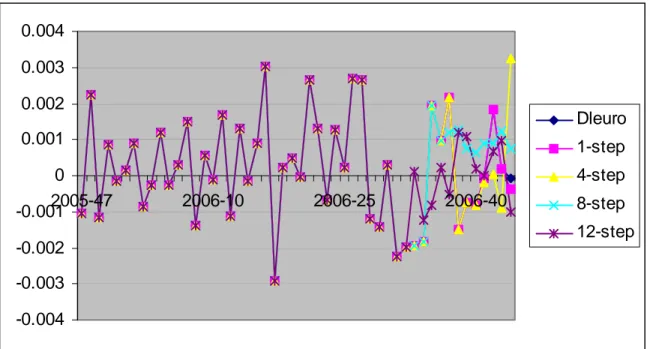

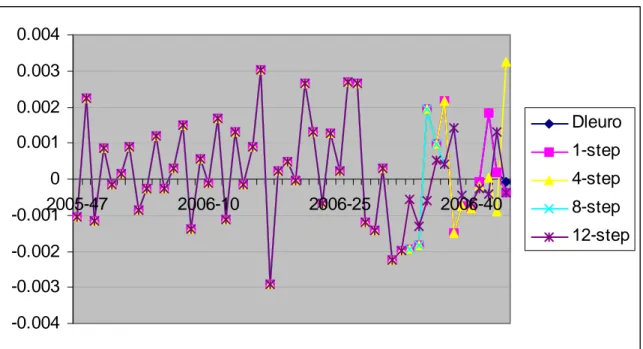

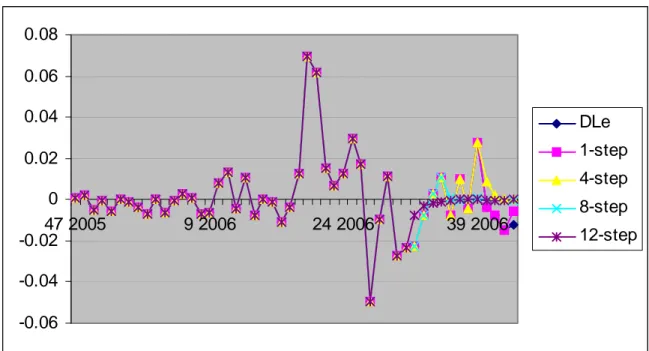

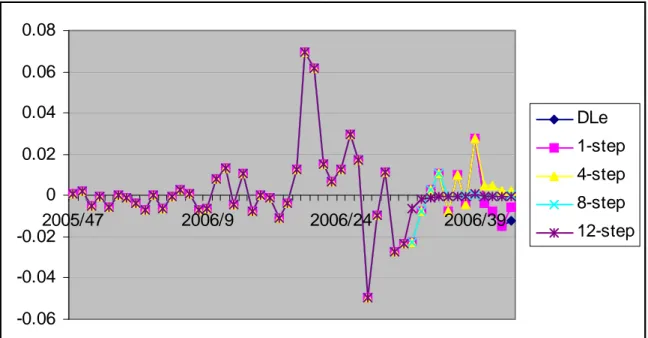

Modelling term structure, exchange rate and interest rate in Turkish economy

Tam metin

Şekil

Benzer Belgeler

in [2] and are suitable for synchronization in digital communi- cation systems without phase ambiguity and with random (PN) frame preamble. The second and third sets are optimized

In a magnetic particle imaging (MPI) scanner, utilizing a tunable gradiometer receive coil can aid in achieving greater degree of decoupling of direct feedthrough signal.. However,

A novel sensing material based on pyrene doped polyethersulfone worm-like structured thin film is developed using a facile techni- que for detection of nitroaromatic explosive

Özel Eğitim Kurumlarında Çalışan Öğretmenlerin İş Doyumu Ve Mesleki Tükenmişlik Düzeylerinin Bazı Değişkenler Açısından İncelenmesi, Yayımlanmamış Yüksek

Bu amaçla ilköğretim altıncı sın ıf düzeyinde kümeler alt öğrenme alanında hazırlanan yaratıcı drama temelli bir matematik ders planı sunulmuştur Bu plan

However, in this paper we examine the issue of Bayesian learning as a direct goal of (one of the) players in a static decision problem and ask the following questions: in

Keywords : Speech coding, lineiir predictive coding, vocal tract parameters, pitch, code excited linear prediction, line spectrum

Furthermore, the number of attached cells was doubled on the non-coated patterned CNT sur- faces when compared to collagen coated patterned surfaces, where collagen coating acted as