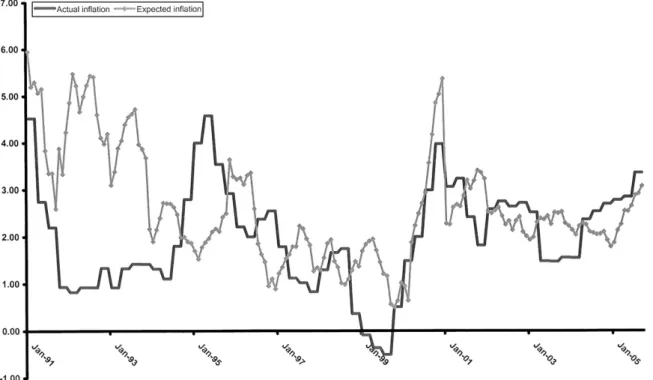

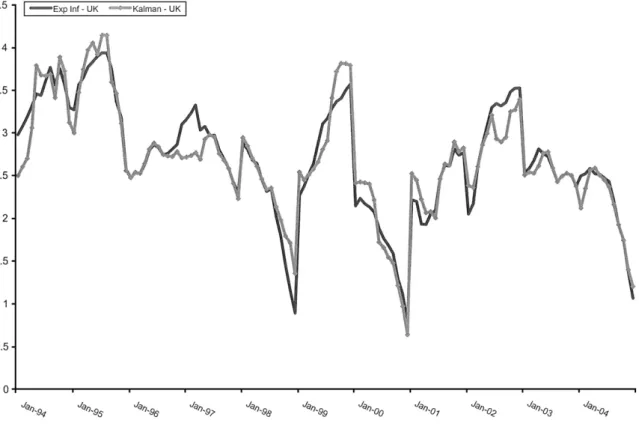

Announcements and credibility under inflation targeting

Tam metin

Şekil

Benzer Belgeler

In this paper, we show that CMUT performance under continuous wave drive signal can be maximized by considering the radiation impedance of the transducer and operating transducer

Our results differ from those of other studies that have investigated the perception of the dress or the perceived illumination of the scene in three ways: (a) Whereas some

We study the exchange and correlation effects on the ground-state properties of dipolar complexes (diplons) formed by the surface electrons on a liquid helium film and positive ions

İkinci Yeni Gerçeküstücülük gibi imgesel olsa da Aragon gibi doğayı bilinçdışı olarak görmediği, şiiri bir “tanıma aygıtı” olarak kullanmadığı

In Section 3, we project out the flow variables in the hub location formulation and characterize the extreme rays of the projection cone for a single

Özetle literatürde incelediğimiz araştırmalara dayalı olarak bu çalışmada teorik açıdan varılan sonuçlar; online ortamda karşılaşılan reklamlara yönelik

In this study, firstly the advertising communication process will be discussed, secondly an attention will be drawn to the importance of content subjects and the use of women image

Kadir Arıcı’nın başkanlığını yürüttüğü “Ahiliğin Günümüz Ticaret Ha- yatına ve Sanayi Sektörüne Kazanımını/ Kazandırılmasını Değerlendirme Grubu”