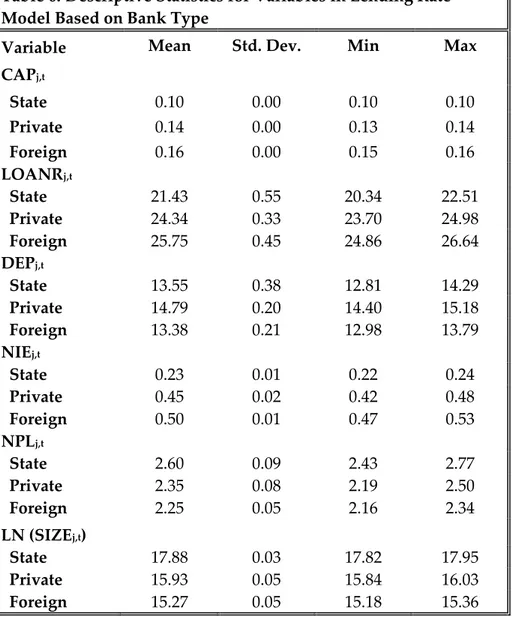

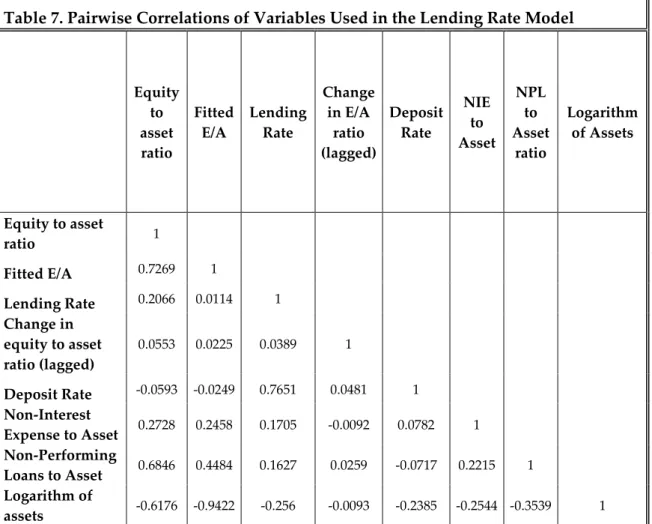

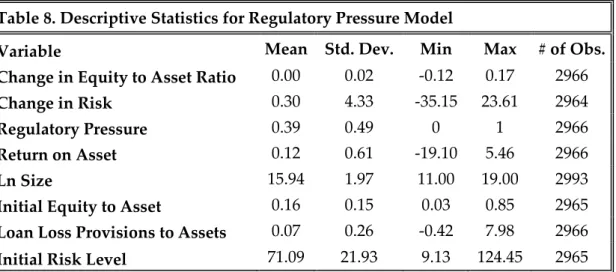

Basel capital requirements and bank behavior : evidence form Turkish banking systems

Tam metin

Şekil

Benzer Belgeler

Pergamon'da Asklepieion'da tiyatro son- daj~ndan gelen lagynos omuz parçalar~~ üzerinde tek merkezli yaprak kom- pozisyonlar~, girlandlar ve müzik aletleri vard~r'''.

Karaman ve ark.'nın geriartik hastalarda yapılan ortopedik cerrahi uygulanan hastalarda yaptıkları bir çalışmada rejyonel anestezi alan grupta yoğun bakımda

Aşağıda tabloda verilen ondalık gösterimlerde işaretlenen sayıların basamak isimlerini, sayı de- ğerlerini ve basamak değerlerini yazınız. Sayı Basamak Adı Sayı

İstanbul vahşi Lûtfi Kırdar umumun menfaati namına Emirgân korusunu üç yüz bin liraya is timlak ederek belediyeye mal etti.. Satvet Lûtfi Tozanın vekili avukat

Yukarıdaki görmüş olduğunuz tablo Şekerci Hacı Bekir'in Maltalı ressam Preziosi tarafından yapılmış ve şu anda Louvre Müzesi'nde bulunan bir tablosu.. Hacı Bekir,

Markanın kullanılması olgusunu, marka sahibi tarafından, yurt içinde, markanın tescil edildiği mal veya hizmetlerde, tescil amacına yönelik, süreklilik arz eden, ciddi,

Genel olarak daha çok Aydın İli Nazilli İlçesi sınırları ve küçük bir kısmının da İzmir İli Beydağ İlçesi sınırları içinde yer alan Oyukbaba dağı ve

In this study, we investigated the distribution of the MDM2 SNP309 genotype and somatic TP53 (the p53 tumor suppres- sor gene) mutations in 99 human HCC samples from Africa,