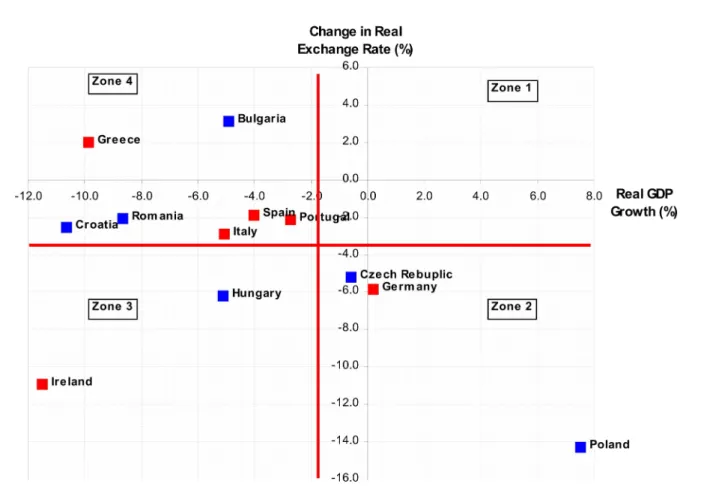

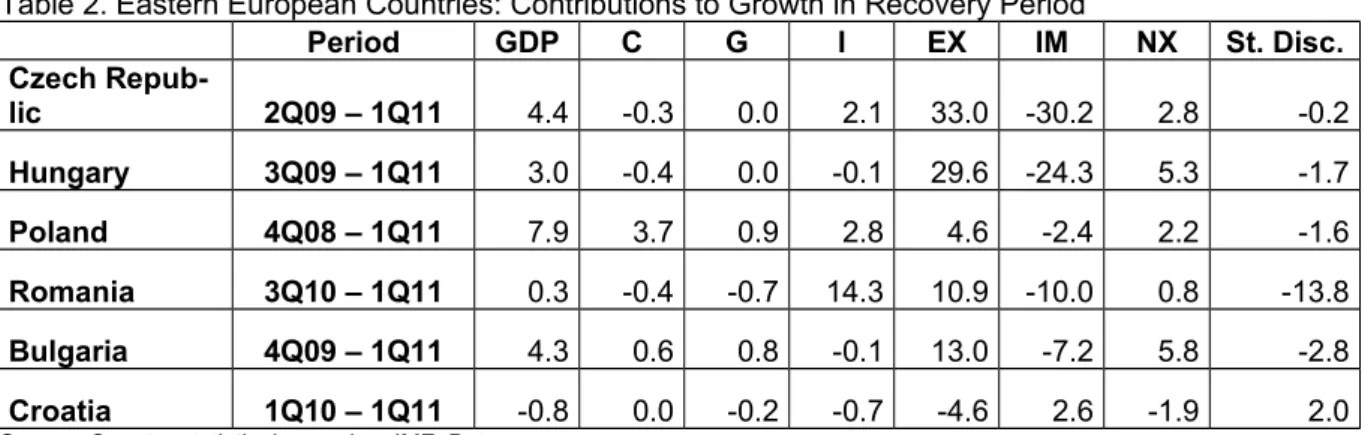

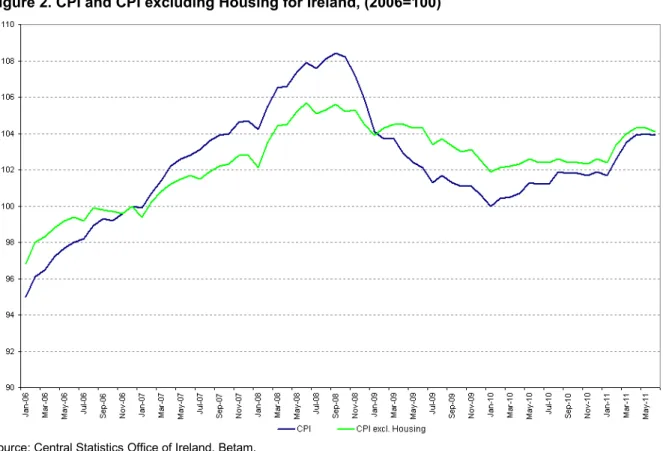

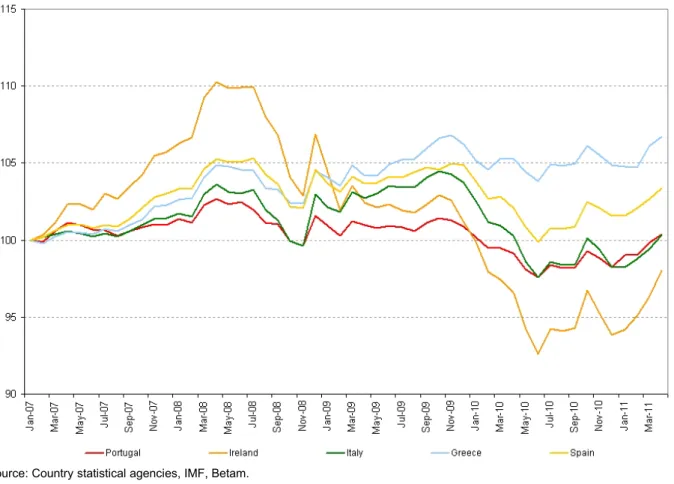

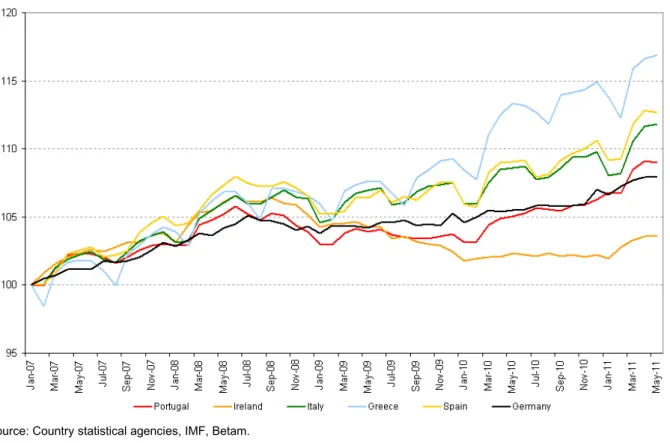

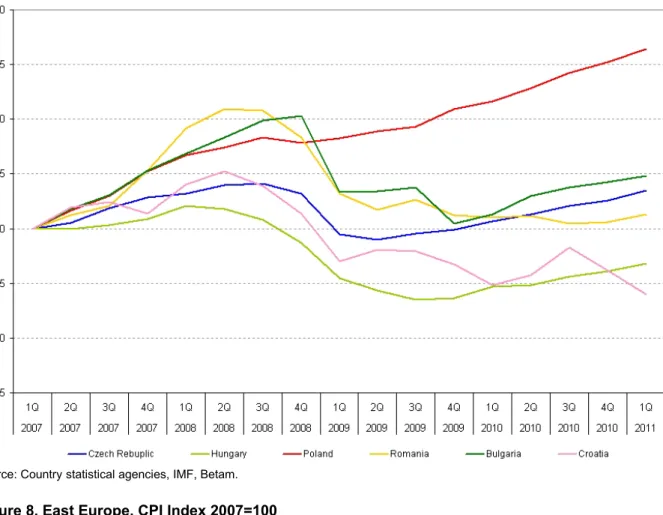

Research brief 11/122 : is euro a fetter?

Tam metin

Şekil

Benzer Belgeler

1897 doğumlu Yücel, bu çatışkının yaşamsal önem kazandığı “M ütareke” döneminde felsefe öğrenimi görerek, düşünen adam kimliği kazanmış

Results: When the patients were investigated in respect of sleep architecture, there was seen to be a significant difference between the two nights in the values of total sleep

Steinbeck takes the reader on a journey to the world of American Dream along with two contrasting characters, George and Lennie, and through this journey, the

My research question is “How does different wavelengths of light affect the rate of germination as measured by observing number of sucessfully germinated seed of Lactuca Sativa

(a) there will be more false recognition when the original information and the misinformation pertain to the same category compared to when they pertain to different

Kalça ekleminin harabiyeti ile sonuçlanan ve hastalarda günlük hayatlarını olumsuz etkileyen şiddetli ağrıya neden olan hastalıkların konservatif tedavilerden yarar

Case report: A rare condition of secondary synovial osteochondromatosis of the shoulder joint in a young female patient. Davis RI, Hamilton A,

Advancing, Ogunleye (2010) recognized that the genuine Exchange rate in the Nigerian economy has been essentially affected by outside stuns coming about because of the ideas of