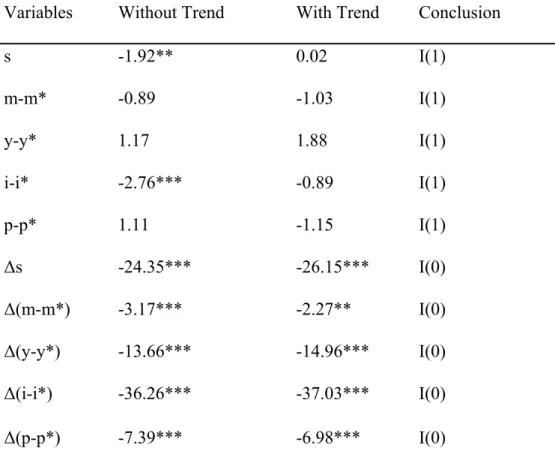

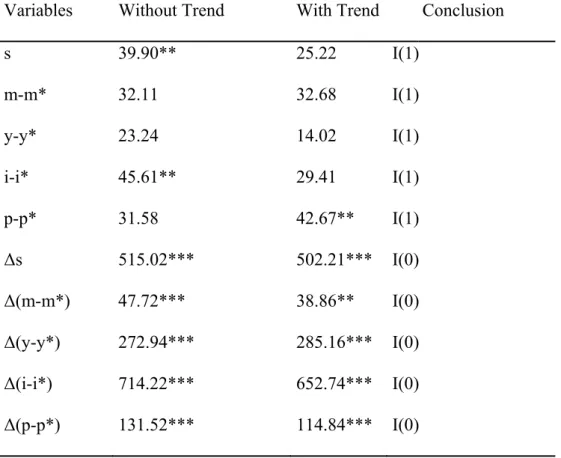

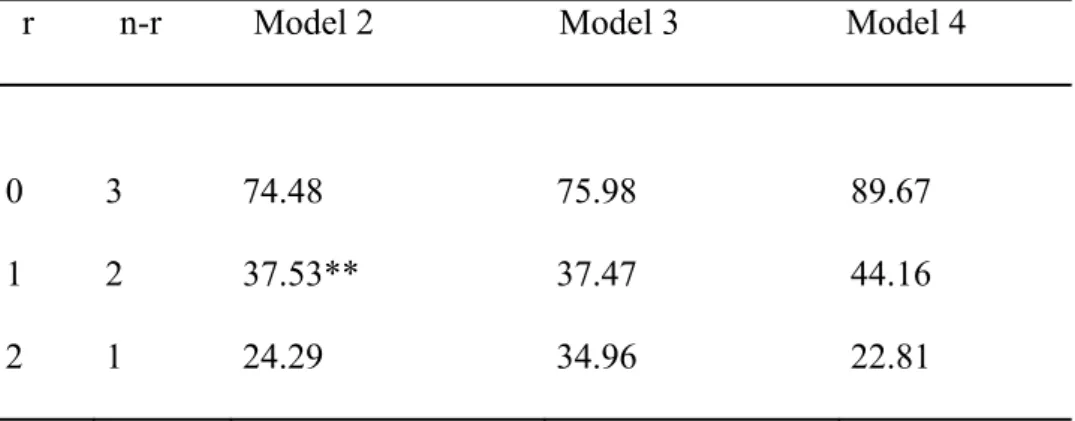

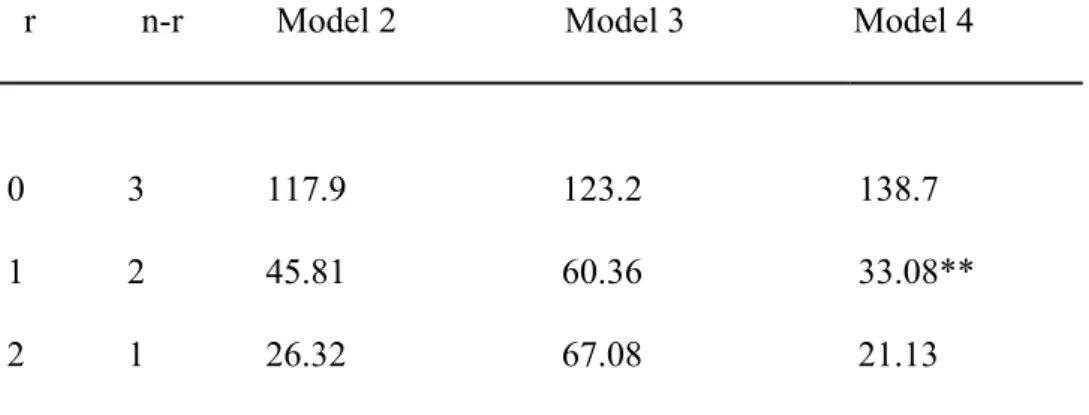

Panel cointegration analysis to exchange rate determination : monetary model versus Taylor rule model

Tam metin

Şekil

Benzer Belgeler

Birbirlerinden ayrılan özellikler de metin içinde geçtiği gibi dekorasyonu, işletmecisiyle bir Rock Bara olan benzerliği ile farklılık gösteren Nektar Bar, kendisine ait

In the third step, four different tourism places in Antalya were distinguished according to their different mix of functions, namely (i) homogeneous tourism places (HOTP’s), (ii)

Sadece genel sa¤l›k alg›lamas› (GSA) de¤erleri yoga grubunda egzersiz grubuna göre daha yüksek bulundu (Tablo 2).Tedavi sonra- s›nda yap›lan de¤erlendirmede, sol ve sa¤

Merkür, ay›n ortalar›nda do- ¤u-kuzeydo¤u ufku üzerinde, gözlenebilecek kadar yükselmifl oluyor.. ‹lerleyen günlerde gezegen yükselmeyi sürdürüyor ve 21 A¤us-

Ahmet Mithat’ın “Çingene” Adlı Romanında Ötekine Duyulan Arzu Üzerine Bir

İnsan beslenmesi açısından oldukça zengin bir gıda olan kinoa, FAO tarafından yapılan karşılaştırmalarda da protein içeriğinin ve kalites- inin, yaygın olarak

Koruma merkezine başvuran çocuklar arasında tütün, alkol ve madde kullanımının yaygın olduğu gözlenmekle birlikte, bu çocukların madde kullanım yaygınlığı ve

Figure 1 shows Main University Campus of Bulent Ecevit University and preferred study area on the high resolution (12 Megapixel) image that we obtained by a UAV