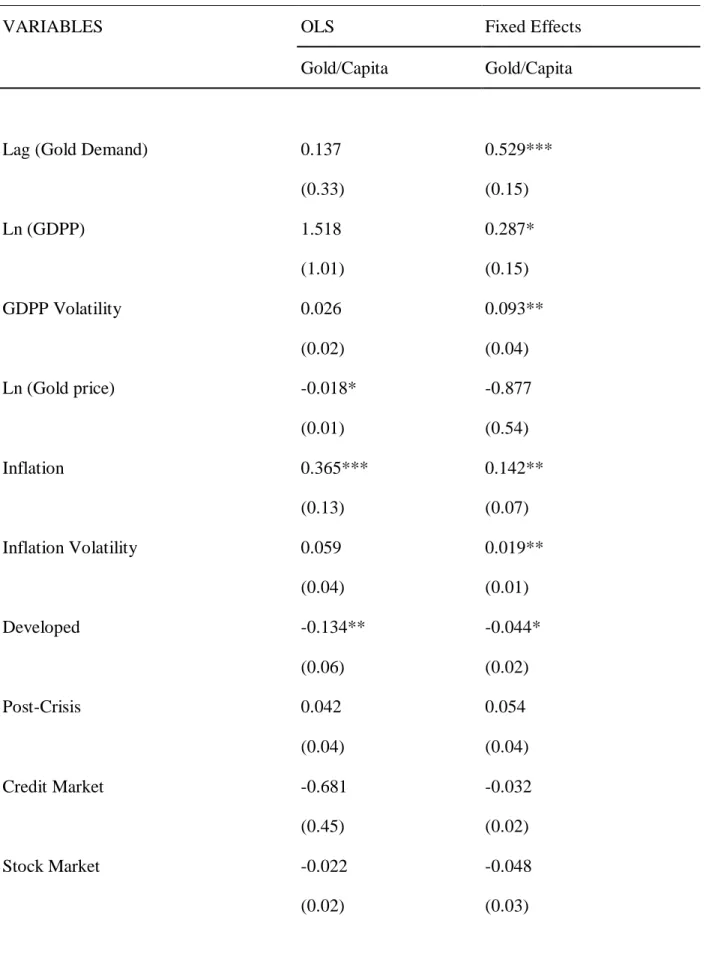

An outlook on determinants of physical gold demand in emerging and developed countries, 2000-20101

Tam metin

Şekil

Benzer Belgeler

Relationship between income and environmental Kuznets curve is examined for developed and developing countries by ARDL model, NARDL model, bootstrap ARDL model and

From the policy development perspective, this study will contribute to the related literature as an original work of modelling external debt, measuring the sensitivity of

While Brazil and Mexico are otherwise grouped with “middle-income countries,” other Latin America countries are repre- sented by 9 studies: pneumococcal conjugate vaccine

Based on the literature review, the theme of improving marketing policies is commonly and equally shared and agreed upon among all these studies. Also, using

Because my research is based on the high-tech industry where firms seek new resources, knowledge, technology, and innovation through cross-border acquisitions, I assume

The aim of the study is to analyze volatility spreads in United States of America (USA), France, Germany, Japan from developed markets and Turkey, China, India, Indonesia

Ali’nin geriye 5 balonu kaldığına göre tüm balonları- nın sayısını gösteren işlem aşağıdakilerden hangisi- dir?. A) 14. Ahmet’in 20 tane daha bilyesi olursa

Bu oteli bitirmek için çok çalışmak gerektiğini, ken disinin de şantiye ş e f i olarak çalıştığını anlatan Vehbi Koç, oteli 6 Eylül 1955’te yapılan “Para Fonu