Performance analysis in Turkish banking sector. Camels application

Tam metin

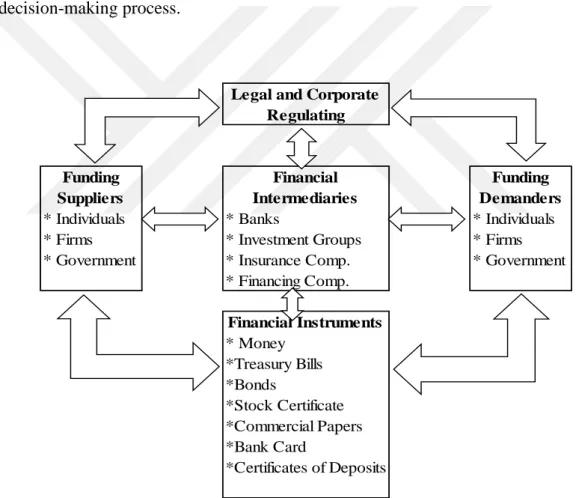

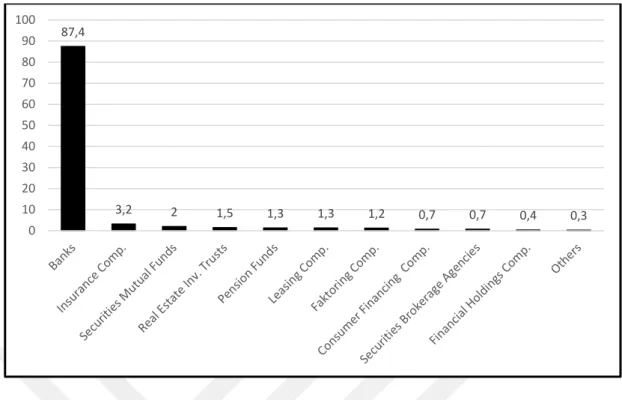

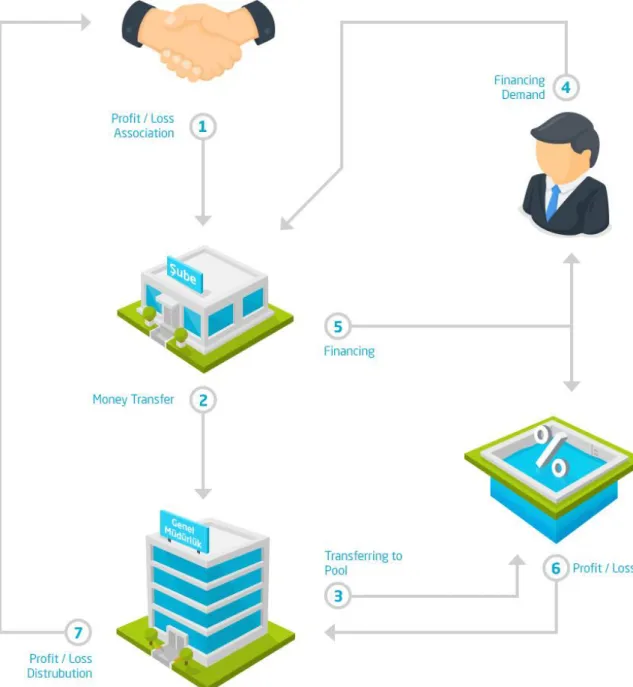

Şekil

Benzer Belgeler

Literatür taramasında ulaşılabilen kaynaklar incelendiğinde, Türkiye’de okul dışı doğa uygulamaları ile desteklenmiş öğretim uygulamalarının öğrencilerin fene ilişkin

Karaman ve ark.'nın geriartik hastalarda yapılan ortopedik cerrahi uygulanan hastalarda yaptıkları bir çalışmada rejyonel anestezi alan grupta yoğun bakımda

Çevresel içerikli sağlık sorunları ile ilgili olarak pil atıkları ve ses kirliliği ile ilgili maddelerde yer alan öğrenci kazanımları “olumsuz etkileri

Bu amaç doğrultusunda, testlerin madde güçlük indeksleri (aynı zamanda her bir maddeye ait başarı oranları olarak ele alınmıştır), ayırıcılık gücü indeksi,

The Arcadian vision and industrial urbanism have together developed a basic cultural premise and produced the most outstanding results since the late nineteenth century – the

Genel olarak daha çok Aydın İli Nazilli İlçesi sınırları ve küçük bir kısmının da İzmir İli Beydağ İlçesi sınırları içinde yer alan Oyukbaba dağı ve

Beyazide doğru derlendiği zaman Firuzağa camiinden sonra gelen büyük bir konak da Bür- hanı Terakki mektebi idi ki zamanının en asrî mektebi saydırdı..

O zamanlar Boğaziçi cennetten bir nümuney- di. Hele mehtab geceleri denizin yüzü seyirci kayıklarile resmi ahnacak bir şekil ve mahiyet teydi. Malûm ya, en güzel