Revisiting the Finance-Growth Nexus in Turkey: Bayer-Hanck Combined Cointegration Approach over the 1970-2016 Period

Tam metin

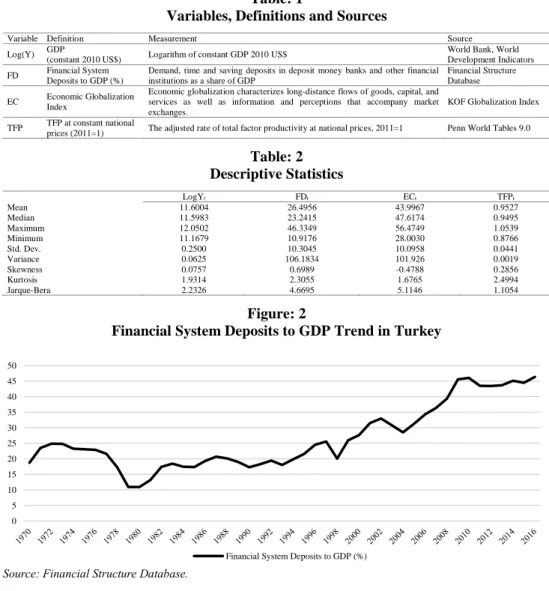

Şekil

Benzer Belgeler

Esasen, kitabın bizim tanıtım yazımıza esas teşkil eden birinci kıs- mının kaynakları olan Dede Garkın belgelerinin hepsi daha önce yayımlanmıştır.. Başbakan- lık

İktisat, kamu yönetimi, işletme, maliye ve sağlık yönetimi alanlarında yazılan makaleler ile özel sayımız bilim insanlarına ve ilgili çevrelere de

According to fig 2.1 the effects of inflation on financial intermediaries is a direct effect but the effect on economic growth in posed in two ways which are efficiency

A combination of oil shocks and a financial crisis poses huge adverse effects on the interaction linking agricultural productivity, oil prices, economic growth and financial... It

Finally, various Granger causality tests in the selected alternative models suggest unidirectional causality that runs from financial sector development to real income

Bu derlemede doğru hücresel fonksiyonları korumak için hasarlı organelleri, protein yığınlarını ve hücre içi patojenleri yok eden bir sitoprotektif program

[r]

The empirical analysis that was carried out in this study reveals that in the case of Nigerian economy, there is an evidence of long run relationship between economic